China Will Transcend Its Demographics

It Will Have the World's Largest Population of Robots

"The factory of the future will have only two employees, a man and a dog. The man will be there to feed the dog. The dog will be there to keep the man from touching the equipment." – Professor Warren Bennis

China now has more industrial robots than the rest of the world combined. Meanwhile, its birth rate just hit a 76-year low. Only one of these facts will determine China’s economic future, and it’s not the one you’ve been hearing about.

Hyped concerns about China’s birth rate treat human labor as the only input that matters for economic output. Anyone with even a passing understanding of the current job market knows that’s not true. Demographics are yesterday’s bottleneck. Today’s bottlenecks are electricity, robots, and supply chains, and China is excelling on every one.

The AI Jobpocalypse

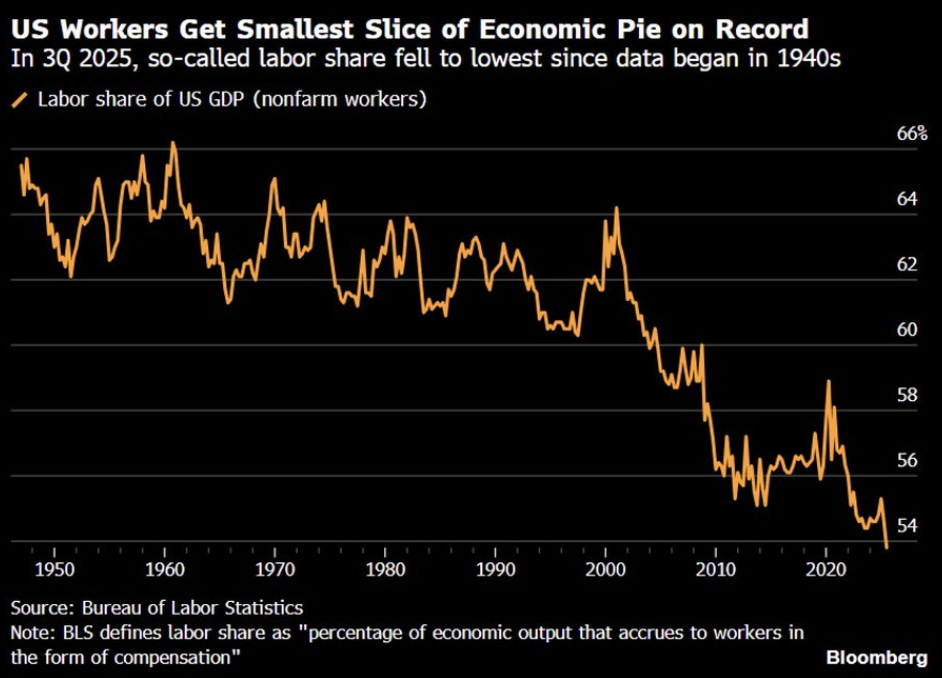

The labor share of US GDP just hit its lowest level on record.1

A summer 2025 survey found that only 30% of that year’s college graduates had secured a full-time job in their field. The unemployment rate for young college graduates has increased much more sharply compared to their non-college-educated peers and the general population.

Companies are not hiring junior employees the way they used to, in spite of the fact that corporate earnings continue to increase.

They just don’t need employees to do tasks that AI can do faster and cheaper. A $380 billion company (Anthropic) operated with a one-person marketing team for 10 months.

In China, youth unemployment has risen to nearly 17%, despite stronger economic growth than expected.

High youth unemployment despite a strong economy is unsurprising once you realize that AI can now do many white-collar tasks faster and cheaper than a junior human employee. And the frontier keeps advancing.

In this world, the hard problem for governments will not be "how do we find enough workers?" It will be "how do we find enough work for the workers we have?"

The Key Inputs: Electricity and Manufacturing Capacity

If economic strength is less about demographics and more about the scale of AI and robotics, then the key inputs are electricity production and manufacturing capacity. On these fronts, China’s dominance is staggering.

1) Electricity Production

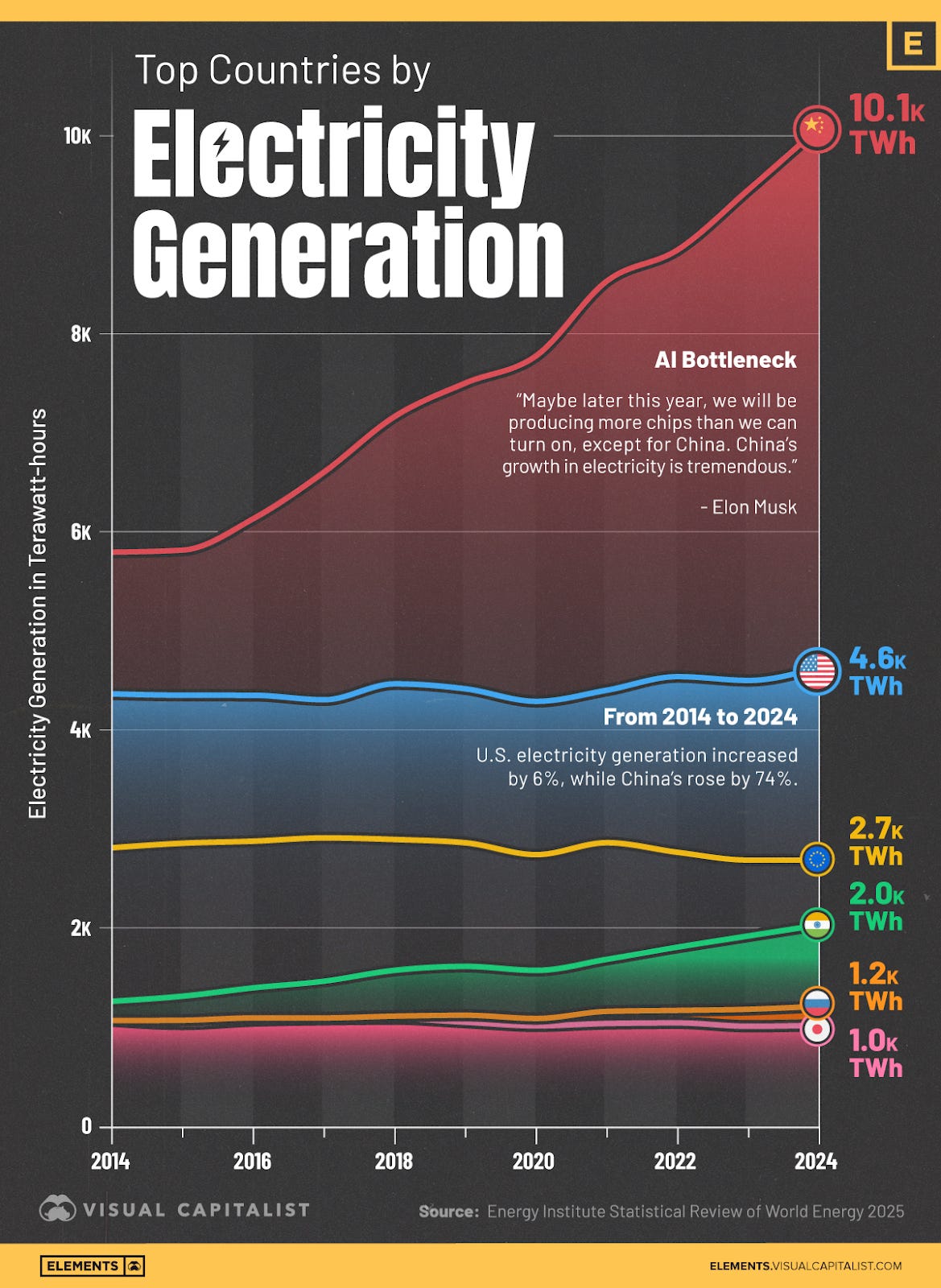

By the end of 2025, China’s total installed electricity generation capacity reached 3.89 terawatts, roughly three times the United States’ 1.3 terawatts. In 2025 alone, China added about 540 gigawatts of new capacity, which is more than the entire installed capacity of India and over eight times the new capacity the US added in the same year2. The gap between US and Chinese electricity production is widening.

Electricity matters because (translated)

“In the future, all critical industries of the future will need electricity. AI and LLM training easily consume millions of kilowatt-hours. Autonomous driving relies entirely on electricity for its massive sensor arrays, cloud computing, and edge processing. Smart cities need power to support everything from streetlights and traffic signals to transportation dispatch and emergency coordination. High-end manufacturing, including wafer fabs and chip plants, demand an extremely stable power supply. The EV revolution hinges on whether the grid can support millions of vehicles charging simultaneously nationwide. In one sentence: the future is a power-intensive society. Without strong electricity infrastructure, the technology of the future cannot exist.”

Jensen Huang of Nvidia has warned that China’s energy subsidies and fewer regulatory hurdles give it a key advantage in AI.

American electricity rates, meanwhile, are skyrocketing under AI-driven demand, with new data center operators waiting up to seven years for grid connections.

In the time it takes a US data center to get a grid connection, China will build roughly 3.8 TW of new electricity generation capacity3, almost three times the entire current US grid.

Elon Musk has said that electricity production is a proxy for industrial capacity. On this metric, China is pulling away at a breathtaking pace.

2) Manufacturing Capacity

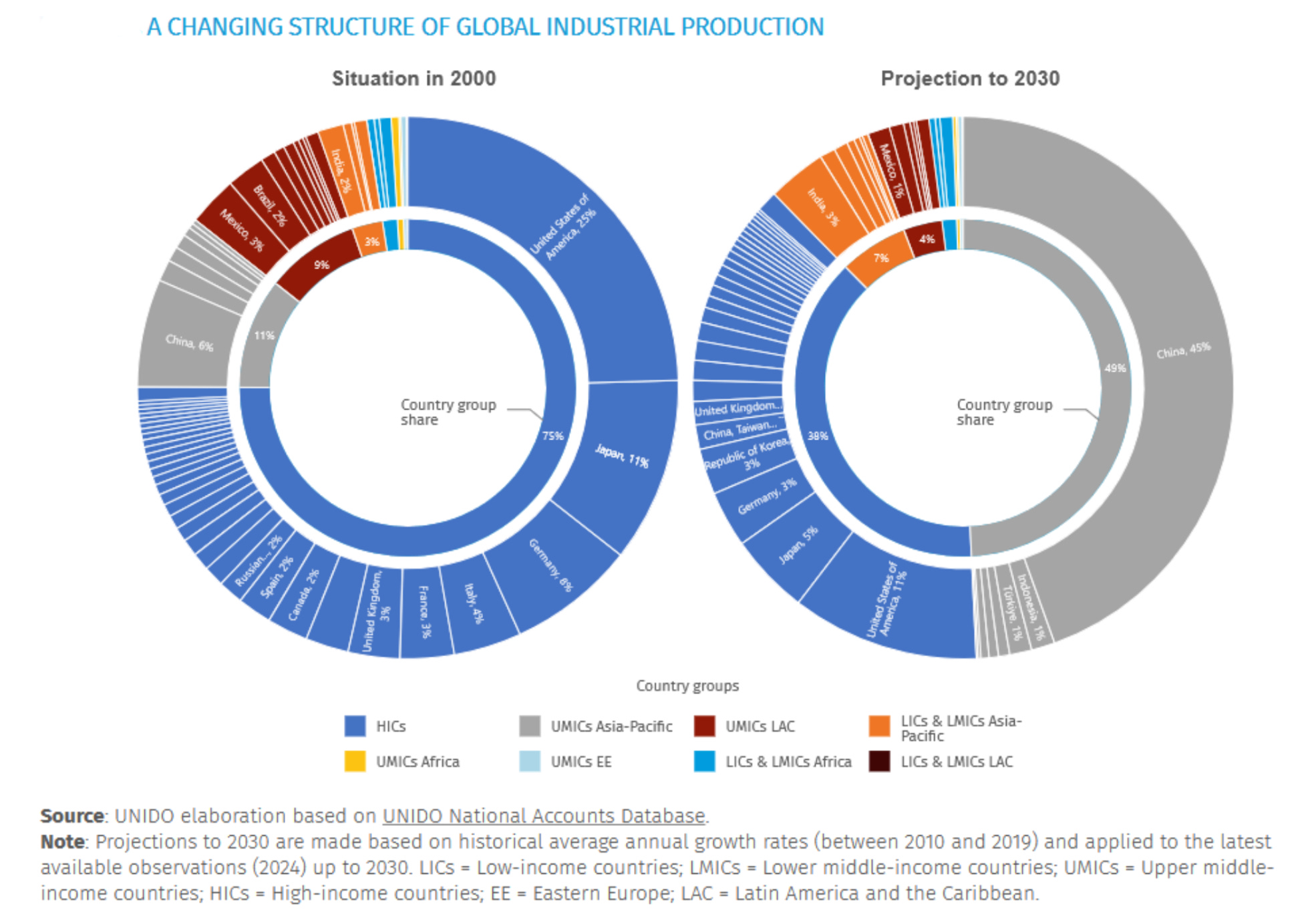

The manufacturing numbers are just as stark. China accounts for about 30% of global manufacturing value added and is on a trajectory to reach 45% by 2030, while the US is projected to fall to 11%.

The Dark Factory and the Robot Army

Generating more electricity than anyone and making more stuff than anyone gives China a massive advantage in robotics manufacturing and deployment.

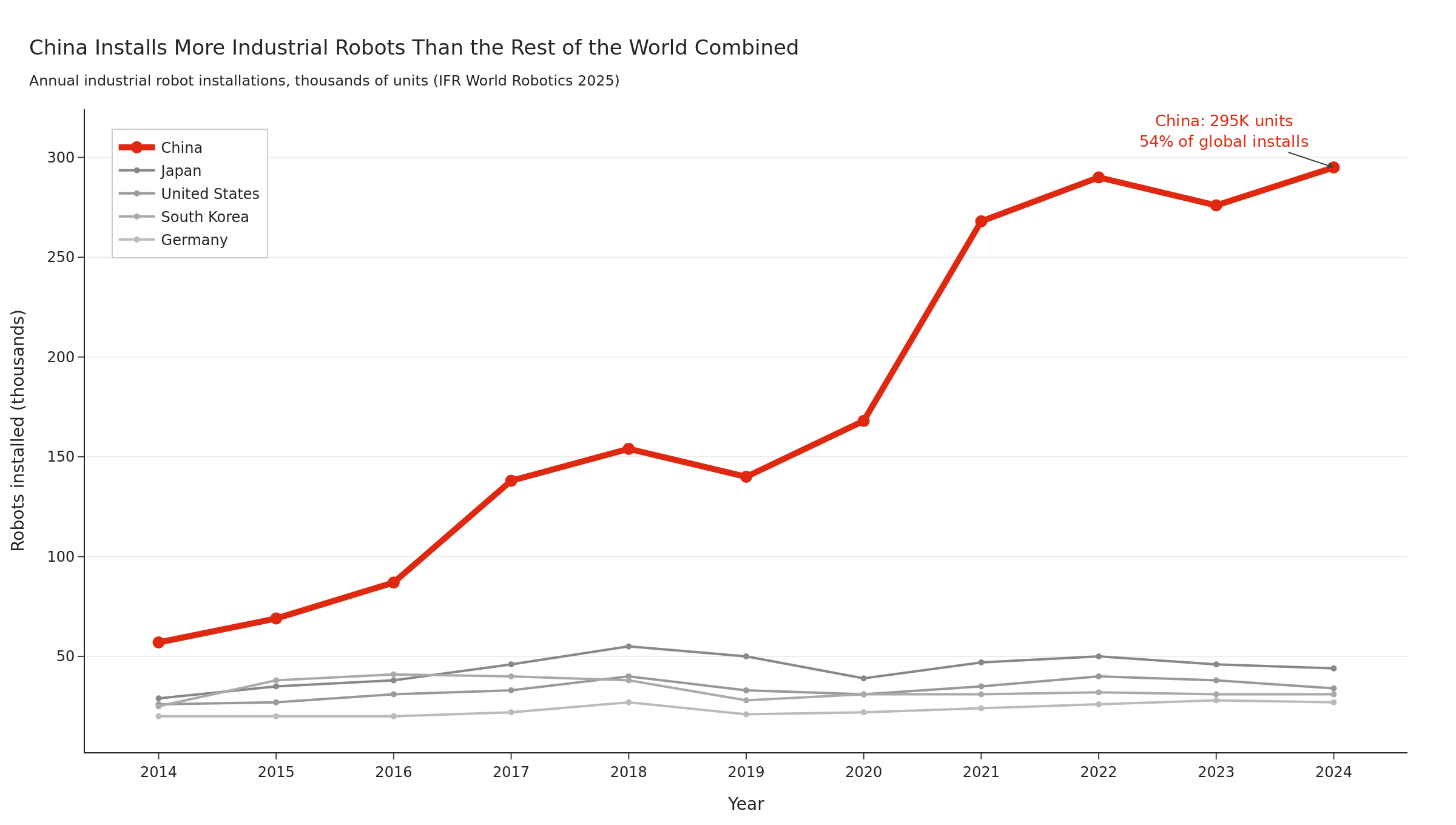

According to the International Federation of Robotics (IFR), China’s operational stock of industrial robots surpassed 2 million units in 2024, a world record. In that year alone, it installed 295,000 new units, representing 54% of global deployments. The number of robots in the country has doubled in just three years. For the first time, Chinese manufacturers sold more robots domestically than foreign suppliers, grabbing a 57% market share.

China now has roughly five times as many industrial robots as the United States, with more industrial robots than the rest of the world combined. The gap is only growing.

Industry forecasts project China’s annual installations rising from 297,000 today to over 533,000 units by 2030, implying an operational stock north of 4 million robots4 by decade’s end. Beijing has put robotics at the heart of its 15th Five-Year Plan.

Today, entire car factories and fulfillment centers are fully automated, and the pace of automation is only accelerating because the cost economics are increasingly favorable. Chinese robotics manufacturers benefit from vertical integration and supply chain density.

“China controls 63% of the key companies in the global supply chain for humanoid-robot components, particularly in actuator parts and rare earth processing. This dominance enables Chinese manufacturers to produce humanoid robots at lower prices than their international competitors. Unitree’s H1 is priced at $90,000—less than half the cost of Boston Dynamics’ Atlas, a comparable model.”

In 2023, when Beijing set milestones for mass production of humanoid robots by 2025 and world leadership by 2027, they knew they had the world’s deepest manufacturing ecosystem to make it happen, and it’s happening.

The country best positioned to build, deploy, and maintain armies of robots is one that will do just fine without a baby boom.

The Dominance of Chinese Manufacturing Clusters

“We don’t make hair dryers. We make the entire ecosystem around hair dryers.” That line, from a Chinese factory boss, captures something the macro numbers miss.

Numbers about electricity and robot installations are useful, but they miss something harder to quantify but even more important: manufacturing clusters and ecosystem density.

Q: Why is every product in China tied to one specific city, e.g. lighters (Wenzhou), Christmas decorations (Yiwu)?

A: In the West, factories are spread out randomly. In China, industries cluster like ecosystems: small home appliances (Cixi), electronics (Shenzhen & Dongguan), toys (Chenghai), socks (Datang), furniture (Foshan), textiles (Keqiao), luggage (Baigou).

This is decades of suppliers, labor, machines, and logistics forming a self-reinforcing ecosystem. Factories don’t move because their entire supply chain is next door.

I once sourced hair dryers for a client. In Cixi, within 5 km, you’ll find motor suppliers, injection molding plants, heater core makers, buttons and shells, packaging companies, and at least 50 assembly factories. One boss said: ‘We don’t make hair dryers. We make the entire ecosystem around hair dryers.’

That’s why a random city in China can outcompete entire countries. Each industry has its capital city. Workers are trained for that product. Machines are optimized for that product. Even the repair shops specialize in that product. When you’re inside the right ecosystem, everything is smoother, faster, and cheaper. When you’re outside it, you’re fighting gravity.

These manufacturing clusters cannot be built with trade barriers alone. These ecosystems developed over decades through a self-reinforcing cycle of specialization, competition, and proximity. Each of these ecosystems has a dense cluster of suppliers, manufacturers, and engineers who collectively know more about making that particular product category than anyone else on earth. Add to this extensive automation and cheap, abundant energy, and it becomes extremely clear how China can dominate global manufacturing for decades to come.

Claude can draft legal briefs and write software. It cannot build factories, let alone manufacturing clusters that contain the physical agglomeration of thousands of specialized firms operating within walking distance of each other. The white-collar disruption from AI is real and significant, but it makes China’s blue-collar infrastructure even more valuable. In a world where software is increasingly commoditized by AI, the scarce resource is the ability to turn ideas into physical products quickly, cheaply, and at scale. No one understands this more than the world’s most valuable consumer electronics company.

Apple Cannot Leave China

If there is a company that should be able to decouple from China, it is Apple. It is a $4 trillion company with more than $120 billion in annual free cash flow. Trade tensions between the US and China have only grown since Apple first established its manufacturing base in China.

Yet 151 of Apple’s top 200 suppliers manufacture in China. Indian-made iPhones are filled with Chinese components.

While Apple has moved some production to India and Vietnam, in Apple’s Q2 2025 earnings call in May 2025, Tim Cook implied this was meant primarily to avoid trade barriers imposed by Washington, noting that Apple customers outside the US would primarily continue to be sold China-made products.

The existing tariffs that apply to Apple today are based on the product’s country of origin as you alluded to. For the June quarter, we do expect the majority of iPhones sold in the U.S. will have India as their country of origin and Vietnam to be the country of origin for almost all iPad, Mac, Apple Watch, and AirPods products sold in the U.S. China would continue to be the country of origin for the vast majority of total product sales outside the U.S.

In March 2026, Tim Cook reiterated that “China is Apple’s most important production base and the primary source of its supply chain.”

If Apple, with all its resources and motivation, cannot meaningfully decouple from China, then it should come as no surprise that major global automakers are exporting cars from China and choosing to leave a lot of money on the table.

Foreign Automakers Now Willingly Give Up Half Their Profits to China

Things are happening that would have been considered absurd a decade ago.

Michael Dunne recounted in The Great China Joint Venture Boomerang:

When I first arrived in China in the 1990s, the deal was simple and brutal. Want access to the world’s largest automotive market? You’ll partner 50/50 with a Chinese company in a joint venture. You’ll surrender half your profits. You’ll transfer your technology. Take it or leave it.

And everyone took it.

But as late as in the 2010s, auto executives made it clear that these joint ventures were solely meant to satisfy Chinese domestic demand.

Western OEMs would not risk becoming dependent on Chinese partners for global production. They would never voluntarily give up 50% of their profits in markets outside China. They’d build dedicated plants in Mexico, Thailand, Eastern Europe – anywhere but China – for their export needs.

That consensus held… until it didn’t.

Foreign automakers are now exporting hundreds of thousands of Chinese-made cars.

GM: 312,000 in 2024, up 65% in two years

Ford: 170,000, up 60% year-on-year

BMW: 110,000; China is its global hub for the electric MINI.

Hyundai: 118,000 in 1H 2025

Renault: 100,000

China’s irresistible manufacturing economics, dense supplier ecosystems, unparalleled manufacturing capacity and scale, abundant electricity, and aggressive automation are so competitive that these Western automakers have rationally concluded that it makes more sense to manufacture in China and give up half of their profits than to build and run plants outside of China and earn 100% of profits.

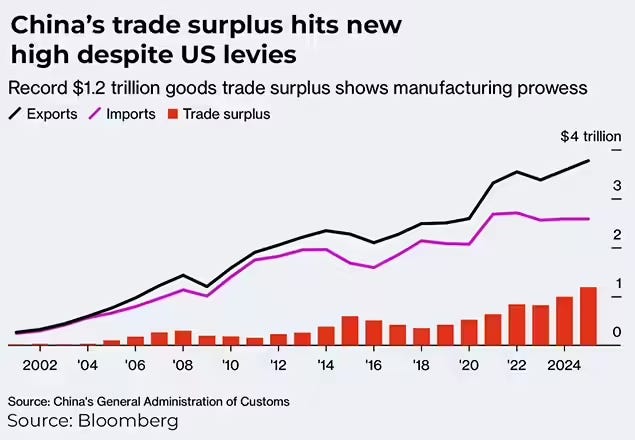

For Apple, Western automakers, biotech, and so many more industries, Chinese industry has become globally irreplaceable, and the best representation of that is China’s enormous trade surplus.

China’s Strategy Is Working

China’s manufacturing dominance led to a record-breaking trade surplus of $1.2 trillion in 2025, the largest by any economy in history.

This was achieved despite US tariffs of up to 145% on Chinese goods, with the US accounting for 23% of that $1.2t surplus.

This year, the momentum has only accelerated: in the first quarter, China’s exports surged almost 12% year-on-year. Chinese manufacturing activity is growing at the fastest pace in the last 12 months. Clean tech exports, particularly solar, EVs, and batteries, have surged in the wake of the Iran war; these were precisely the sectors that had previously had the greatest overcapacity.

Despite the best efforts of Washington politicians, structural economic forces keep pulling the US and China together.

The reason is simple. Manufacturing is a tough, low-margin business compared with designing chips (Nvidia), selling online ads (Google, Meta), writing software (Microsoft), or retailing (Amazon). Americans just don’t want to work in factories. But someone has to.

China wins on cost, time, and quality simultaneously because of cheap energy, manufacturing clusters, automation, and zeroth-world infrastructure for moving components to wherever they need to be.

No Plaza Accord This Time

China today commands an even larger manufacturing edge5 than Japan did in 1985, when Washington forced up the value of the yen and killed Japan’s cost advantage.

In 1985, the United States strong-armed Japan into the Plaza Accord. Japan was a treaty ally, dependent on American security guarantees, and ultimately willing to comply under diplomatic pressure.

The consequences were catastrophic. The yen doubled in value against the dollar, making Japanese exports, the engine of its economy, uncompetitive globally.

The Bank of Japan slashed interest rates to compensate, inflating the most spectacular asset bubble in modern history. When it popped, Japan entered the economic stagnation of the Lost Decades.

China is not Japan. It is not a US treaty ally. It does not depend on American security guarantees. And even US intelligence now reluctantly agrees China will not invade Taiwan. China controls its own currency. There is no conceivable diplomatic framework under which Beijing voluntarily accepts a massive RMB appreciation to satisfy Washington.

The modern equivalent of currency pressure is semiconductor export controls, but where Huawei trails Nvidia on advanced chips, it is closing the gap via cluster-level architecture. As Doomberg puts it:

Although even Huawei acknowledges that its AI chips trail Nvidia’s best offerings by approximately one generation, the company is closing the performance gap through innovative computing architectures and can now meet or even exceed Nvidia’s cluster-scale performance. This is akin to designing a car to have better overall performance through superior aerodynamics, lighter weight, a better transmission, and an optimized drivetrain, despite having a slightly inferior engine. Your engine might have more horsepower or sip less fuel in bench testing, but in the end, it is performance on the track that matters most.

A cheap RMB helps China solve its debt problem (300% debt to GDP ratio). Exporters earn in more valuable foreign currencies while the vast, vast majority6 of domestic debts are denominated in cheaper renminbi, whose monetary policy Beijing fully controls.

Without the world’s dominant reserve currency, China cannot print dollars to fund its way out of a property crash the way the US did after 2008. But as the world’s dominant manufacturing powerhouse, it can print goods and sell them to the rest of the world, and that’s exactly what it’s doing.

The Bet

Xi Jinping is making a large, calculated bet on high-tech manufacturing. The bet is that AI and robotics, enabled by the world’s largest manufacturing base and the world’s largest electricity grid, can raise the output of every remaining worker enough to overcome demographic headwinds. Each of China’s specialized city ecosystems will integrate the highest levels of automation and technical sophistication for its respective product category. The dark factory, staffed by robots and monitored by a handful of engineers, will be the norm.

If you believe that AI will do more and more white-collar work and robots will do more and more blue-collar work, then the relevant question for national competitiveness is not “how many babies are being born?” It is “who can build and deploy the most robots, powered by the most electricity, integrated into the deepest manufacturing ecosystems?”

On every one of those metrics, the answer is China.

Consumption in an Automated World

The same forces that let China transcend its demographics will force every economy to confront the question of who will consume. Given that robots don’t consume, people are right to question how the economy would work if it was significantly more automated.

The stark reality today is that almost half of consumer spending comes from the top 10%, and that share is likely to continue to rise.

Alex Imas’ Substack article What will be scarce? describes exactly the way the top 10% will consume in a post-AI world.

People in developed economies often pay more for objects than what they’re worth in a functional sense. One of his examples is an Armani suit. Nobody who buys Armani is buying a better way to keep warm. They’re buying the brand, the relationship to the story behind Armani, its meaning, its reputation, the fact that other people know what it is and want it. Hickey’s point is that desire is not just based on what products but also what they mean.

Imas is exactly right, and he just so happens to be perfectly describing the consumption habits in our modern K-shaped economy, “where asset-owning classes have become ever wealthier while lower-income households have seen their living standards stagnate or decline.”

In Shreve, Crump & Low, a jewellery store in Greenwich, Connecticut, a Laurent Ferrier “Grand Sport Tourbillon” watch can set you back as much as $210,000. Business is brisk. […] “Demand has actually increased over the past six months.”

In the city of Bridgeport, a 30-minute drive away, demand is also rising — but for a different kind of product. People here are flocking to the city’s food pantries and soup kitchens as the high cost of living bears down on lower-income families.

Imas likened the job displacement caused by the rise of AI to the decline in employment in agriculture in the 20th century.

Economics has a name for what happens when a new technology makes one sector dramatically more productive: structural change. The canonical example is agriculture. In 1900, about 40% of the American workforce was employed in farming. Today it’s less than 2%. Did people stop eating? No, if anything they’re eating much more. Large scale automation made farmers—and eventually factory farms—much more productive. Agricultural production boomed and prices fell. But because people can only eat so much, the share of income spent on food went down as people got richer, and workers moved to manufacturing and then to services.

Ultimately, there is a huge difference between the 1900s’ mechanization of agriculture and today’s AI boom.

Agricultural automation displaced workers at the bottom of the income distribution, who moved from rural farms into cities for higher-paying factory and service jobs7.

AI inverts this: it displaces workers in the upper-middle of the distribution, with no higher rung to climb to. Every adjacent ‘safer’ job (plumbing, nursing, skilled trades) pays less than the knowledge work being destroyed.

Prediction: In the future, wealth inequality, exacerbated by AI and robots, will be a much bigger problem than the lack of human labor.

About

Inverteum Limited (HK) is a trading firm that specializes in long-short algorithmic strategies to generate returns in both bull and bear markets.

Inverteum has generated 50%+ annualized returns since inception.

How We Invest

Minimize allocation to individual stocks due to their unpredictability

Build a strategy designed to harness the market’s momentum, with the tactical agility to pivot and capitalize on downward trends when necessary.

Be prepared for bear markets and ensure profitability during bad times by implementing a short selling component to the strategy

China’s data doesn’t go as far back as the US, but even there, the labor share of GDP has hit lows not seen since the financial crisis.

“In the United States, the Energy Information Administration (EIA) projected about 63 GW of new utility-scale generating capacity additions for 2025 across all technologies.”

Per China’s National Energy Administration, China saw “net additions of roughly 540 GW in a single year” in 2025. At that pace over a 7-year period, China would add 540 GW × 7 ≈ 3.78 TW of new capacity. 3.8 TW is a low-end estimate given that annual additions have been accelerating year-over-year.

2024 operational stock of 2.03M robots + sum of installs 2025-2030 at Next Move Strategy’s 12.4% CAGR (297K + 334K + 376K + 422K + 474K + 533K ≈ 2.44M new units) − approximately 0.4M retirements (IFR assumes a 12-year service life, so robots installed in 2013 and earlier start retiring during this window) ≈ 4.0M operational stock by end of 2030.

China is projected to reach 45% of global manufacturing value-added by 2030, far beyond anything Japan ever approached.

Just US$1 trillion of China’s debt is not denominated in RMB. “The outstanding external debt in foreign currencies (including SDR allocation) totaled RMB 7286.4 billion (equivalent to USD 1036.6 billion)”. For a $21 trillion economy, that means that debt not denominated in RMB is less than 5% of GDP.

Britannica: “The rising demand for manufactured goods meant that average people could make their fortunes in cities as factory employees and as employees of businesses that supported the factories, which paid better wages than farm-related positions.”

Thank you for this work. Question for you after reading… As the West pursues "de-risking" and "friend-shoring," can China’s localized clusters survive a decoupled world where they lose access to high-end Western chips or specific consumer markets in Europe and North America? Can a "robot army" innovate at the frontier, or is it better suited for perfecting existing manufacturing processes?

Outstanding article.

Confirms, again, the kind of momentum that China is attaining and the force, scale, and forward directed vision of where they want to go.

Compared to the exhausted ideals of the western countries and the sense of contested political narratives competing for pro-business vs sustainability agendas at odds with each other about the way forward, the contrast is stark.

The West thinks it can contain China and even derail or dominate. Seems like China might just steamroll and flatten the once dominant western order if the ruling classes don't pick up the pace and embrace the scale of the challenge. Not because of Chinese malice, but because they are going breakneck speed in their own direction of developing the global South when the West falters.

Amazing how China has done so well in such a short time, relatively speaking.