America Will Keep Succeeding

It has 50 one-party states and a federal government that a ham sandwich can lead

Washington is dysfunctional, the national debt is spiraling, and the culture wars are at a fever pitch. From outside observers to the average voter, almost everyone agrees on one thing: the American political system is broken. It is a bipartisan article of faith that the country is in decline. And yet, through it all, the US economy keeps crushing the rest of the developed world.

Time to Sell America?

“There’s one American stock I never thought I would sell,” Nomad Capitalist said in April 2026. “That company is Berkshire Hathaway.” Now, he is selling all his US investments, including Berkshire.

Nomad Capitalist’s “sell America” thesis is based on both parties turning against free markets, with populism, crony capitalism, golden shares, and explicit pressure on companies over buybacks, pricing, and executive pay. In his view, this threatens regulated, domestically exposed businesses like railroads, utilities, insurance, and real estate inside Berkshire, so he is even selling BRK, which he once saw as a core long‑term holding.

Nomad Capitalist is reallocating from American companies to Japanese trading companies and other emerging market names, arguing that they are better positioned to win while also providing foreign‑currency diversification away from the US dollar. It is the logical conclusion of watching too much cable news, and it is wrong. He is a smart consultant making a bad bet because he has misread the US system. The forces he cites are real, but they do not threaten American prosperity.

Nomad Capitalist is wrong about America’s decline

America’s federal architecture is the most durable engine of economic dynamism the world has produced, and it will keep the country succeeding. The argument is simple:

The federal government is both interchangeable and limited in power, as much of the governance is executed at the state level. Because control of the White House and Congress shifts every four to eight years, no single administration can durably alter the nation’s economic trajectory.

Each state, by contrast, can be a lasting one-party regime. California has been blue and Texas red for generations, giving each decades of uninterrupted policy continuity.

That continuity lets each state compound a flywheel: Texas builds energy abundance, California builds the world’s richest pool of technical talent. These advantages accumulate precisely because no election cycle resets them.

The states then trade with and offset each other’s weaknesses, giving America a diversified portfolio of fifty compounding economies whose prosperity can continue into the future.

The Country That a Ham Sandwich Can Lead

“Buy into a business that’s doing so well an idiot could run it, because sooner or later, one will.” - Warren Buffett

That is Buffett’s famous investment test. His biography The Snowball (p. 678) recounts:

I always used to tell [Bill] Gates that a ham sandwich could run Coca-Cola. And it was a damn good thing, too, because we had a period there a couple of years ago where, if it hadn’t been that great of a business, it might not have survived.

Buffett’s point: durable franchises survive incompetent management. In today’s hyper-competitive economy, very few private businesses are strong enough to meet that bar. Even Coca-Cola now needs at least adequate management to thrive, given declining soda consumption.

The United States federal government, by contrast, passes Buffett’s ham-sandwich test with flying colors. At all times, 100% of the country is convinced that either the current or former president is or was a ham sandwich. And yet, under Obama, Trump 1, Biden, and Trump 2, the US economy has grown.

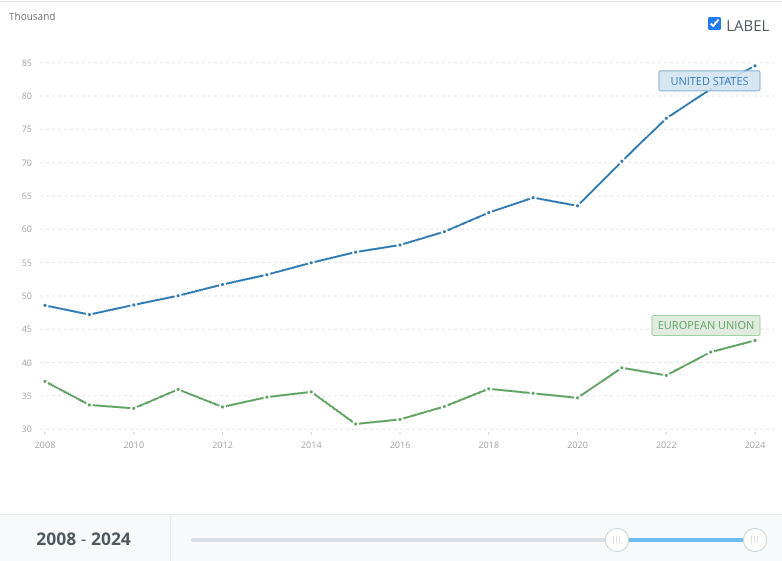

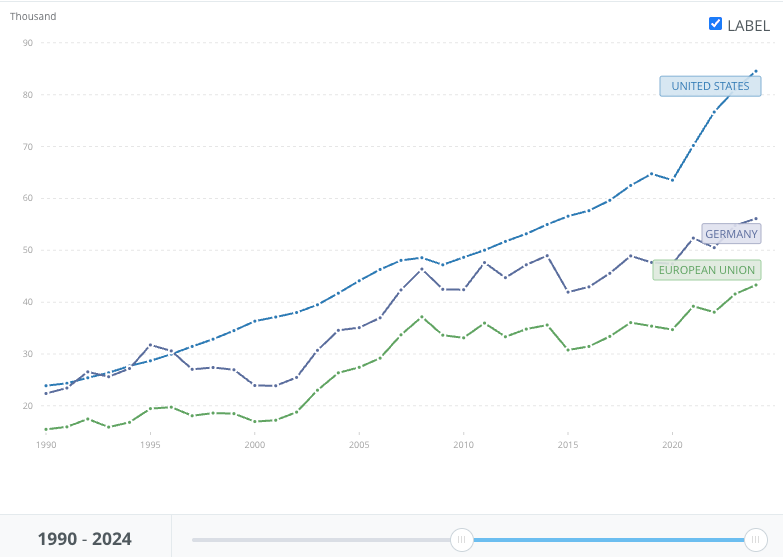

At the same time, EU GDP per capita fell from 76.5% of US GDP per capita in 2008 to 50% in 2023, with the gap continuing to widen. Through three presidents widely derided as unqualified by their opposition, as well as multiple government shutdowns, America has extended its lead over the rest of the developed world.

This is because federal dysfunction is largely irrelevant to where American prosperity is actually produced.

Why American Federalism Outperforms European Parliamentary Systems

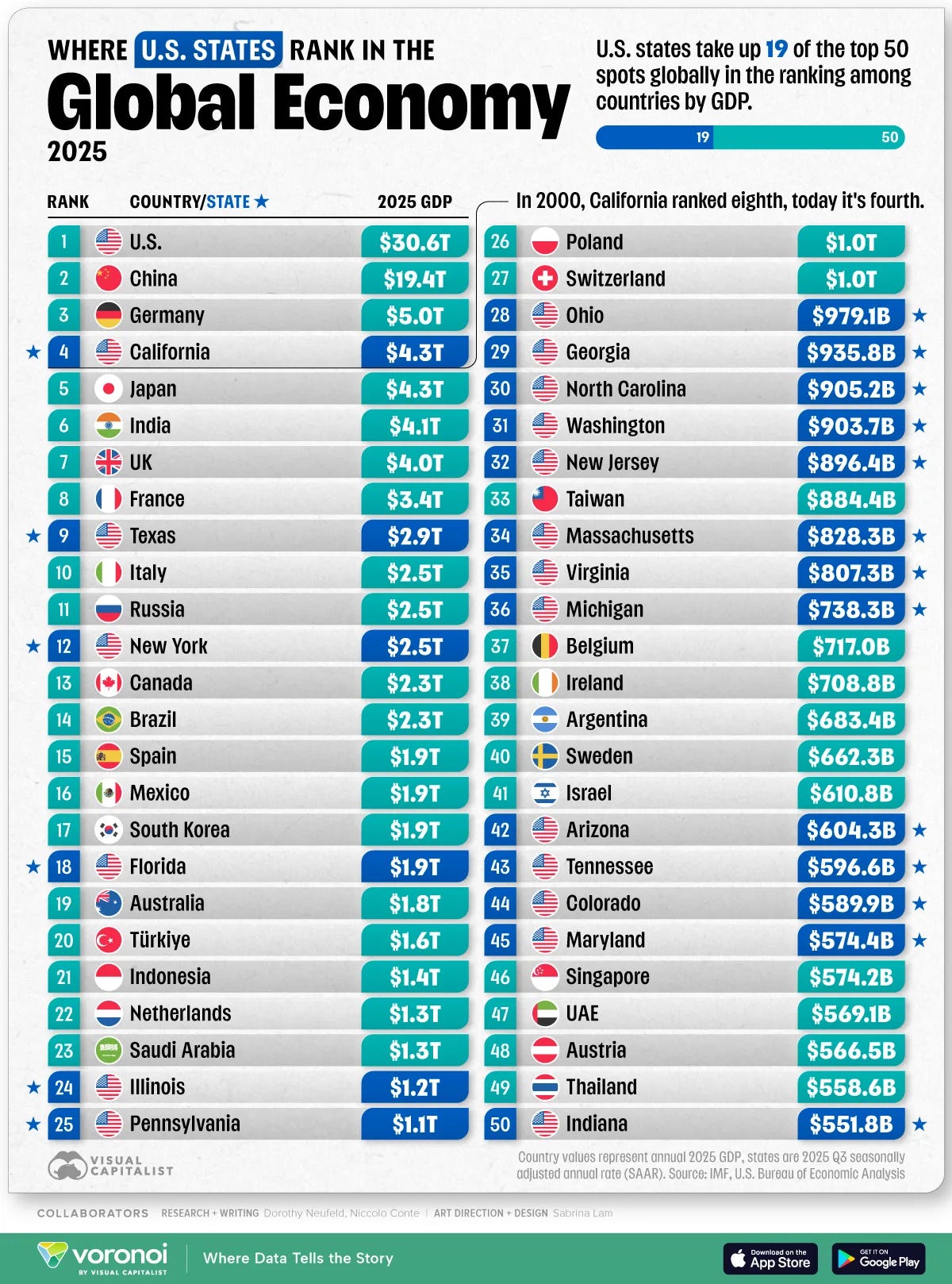

Prosperity is produced in the states, and this is where America’s true advantage lies. American federalism quietly accomplishes what no parliamentary system can. While the federal government lurches between parties every four or eight years, individual states are dominated, often for decades, by a single party. California has been governed by Democrats for over a generation. Texas has been governed by Republicans for nearly as long. Florida has trended deep red; Massachusetts and New York reliably blue. The result is that even when the White House and Congress changes hands, the policy environment in any given state remains remarkably stable.

This stability is primarily caused by first-past-the-post, winner-take-all elections, which journalist Max Fisher shows inevitably lead to

a two-party system

tyranny of the majority by the dominant party in that area.

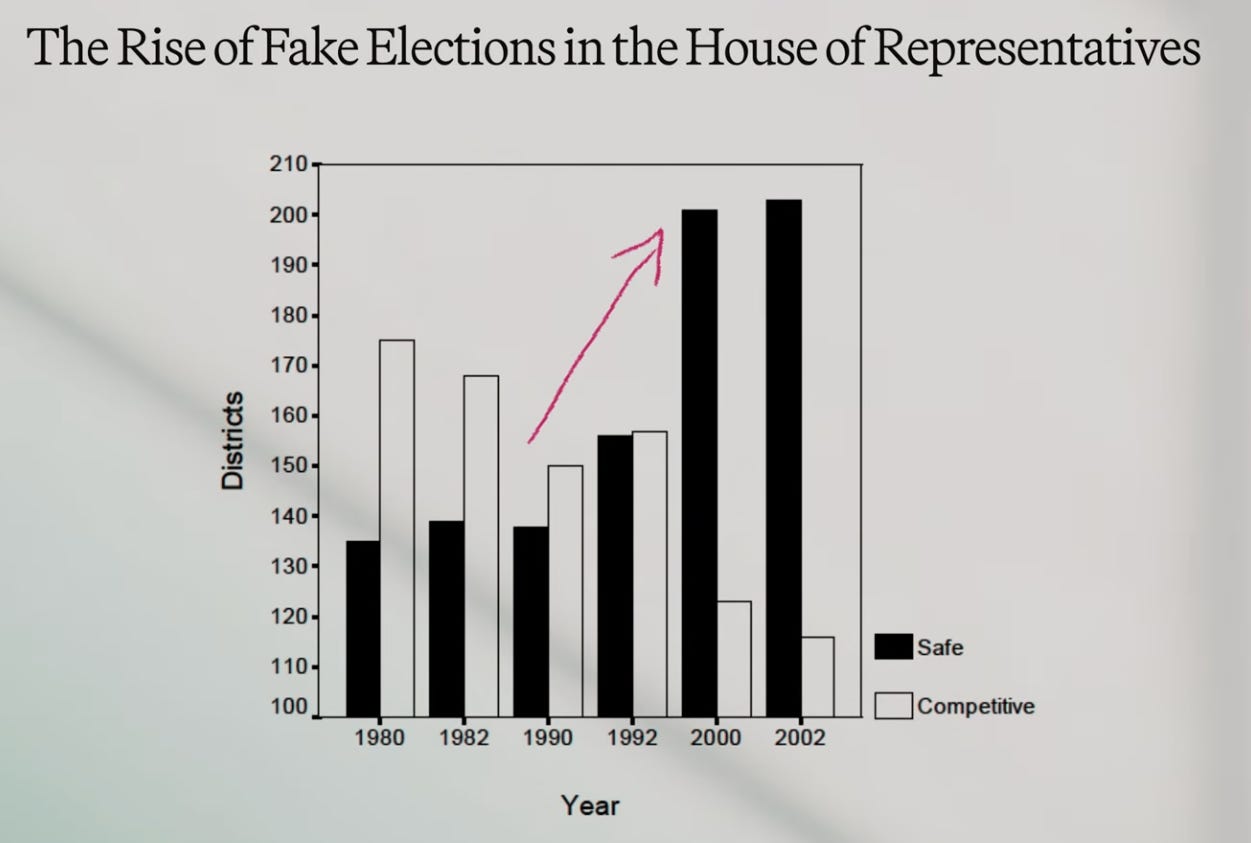

Fisher argues that this makes most US elections meaningless, as whichever candidate gets the dominant party’s nomination in that district or state automatically gets into office. He notes that starting in the 1990s, elections for the House of Representatives went from being mostly competitive to mostly safe, or “fake”, in his parlance.

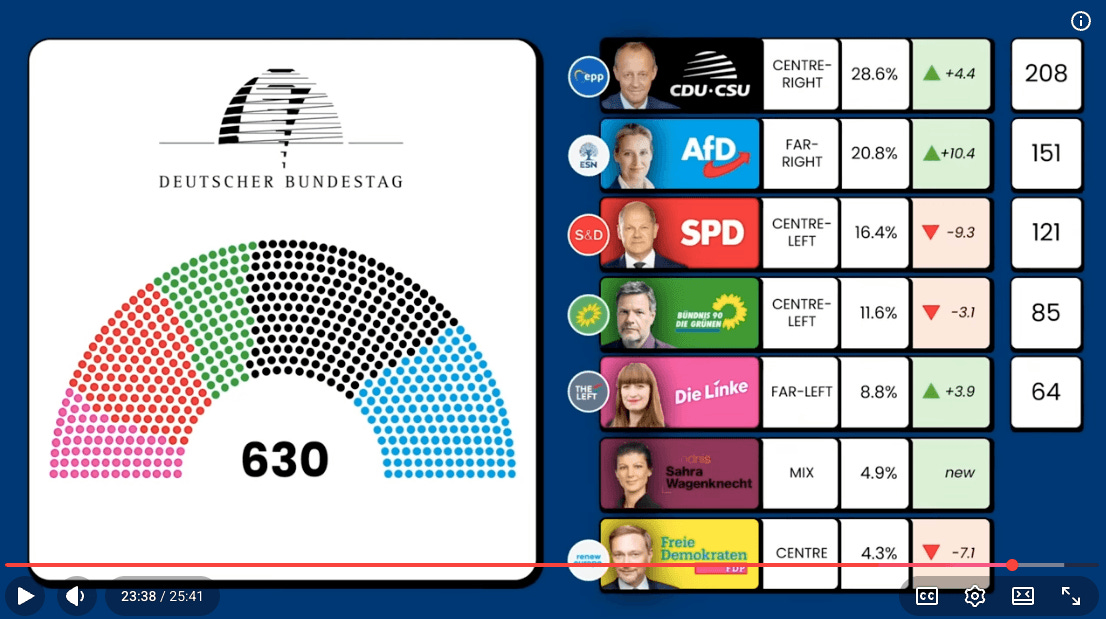

To make the US more “democratic,” Fisher argues that the country should adopt proportional representation, as it exists in Germany and other European democracies.

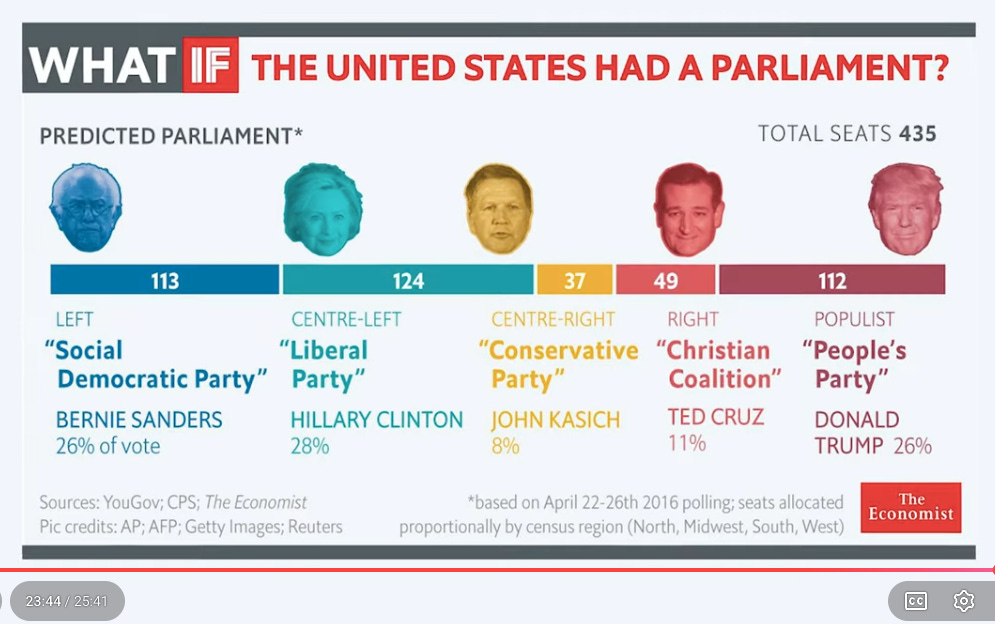

In these parliamentary systems, there are several political parties and the largest coalition governs. Here’s a hypothetical set of US political parties under this system:

Putting aside the fact that implementing such a parliamentary system in the US would require both dominant political parties to voluntarily give up power (which they would never do), it would also mean trading away the state-level policy continuity that gives the US its decisive economic advantage over those exact parliamentary systems.

Starting around the same time that US elections became “fake” in the 1990s, the US went from having similar per-capita output as Europe to becoming significantly more prosperous than Europe.

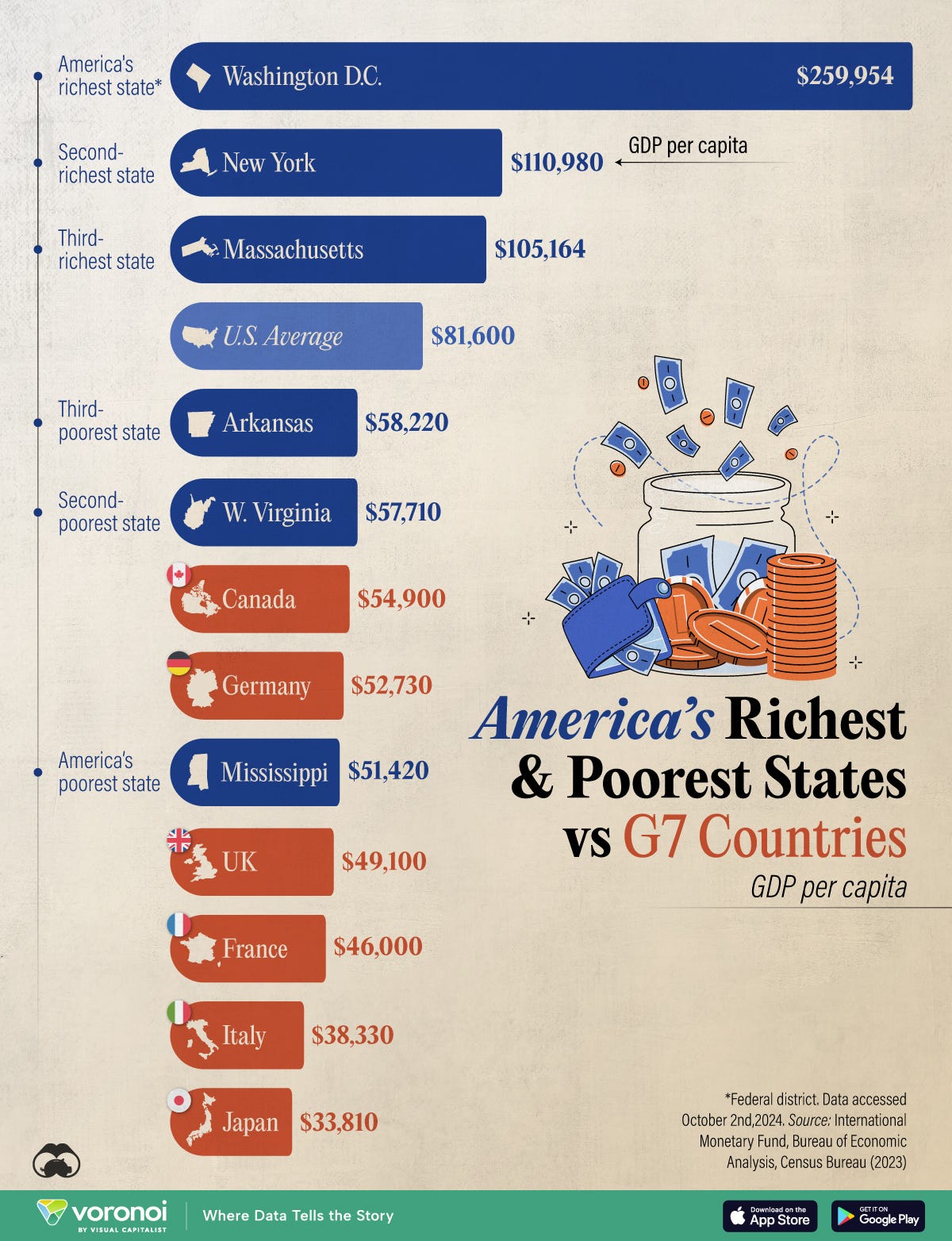

Today, the second poorest US state, West Virginia, has a higher GDP per capita than every other G7 country, none of which have a US-style two-party political duopoly.

Economies ruled by parliamentary governments lag behind America because their ruling parties must constantly cut deals to maintain fragile governing coalitions; this inevitably leads to detrimental long-term policies driven by flavor-of-the-month public opinion.

Germany’s Cautionary Tale

In 2011, Angela Merkel ordered the shutdown of all of Germany’s nuclear power plants by 2022 to help her stay in power.

Angela Merkel’s bid to outflank the opposition by closing all nuclear plants by 2022 smacks of opportunism to many Germans but could ease an alliance with the anti-nuclear Greens that may be her best bet to stay in power. [...]

With opinion polls showing categorically that most Germans dislike nuclear energy, and election results demonstrating that March’s nuclear moratorium alone was not enough to stem the vote losses for the CDU, Merkel probably had no choice.

This is in spite of the fact that at the time, the President of the Federation of German Industries (BDI) warned that the rushed nuclear exit would backfire:

If power supply can no longer be guaranteed, it will weaken Germany as an industrial nation.

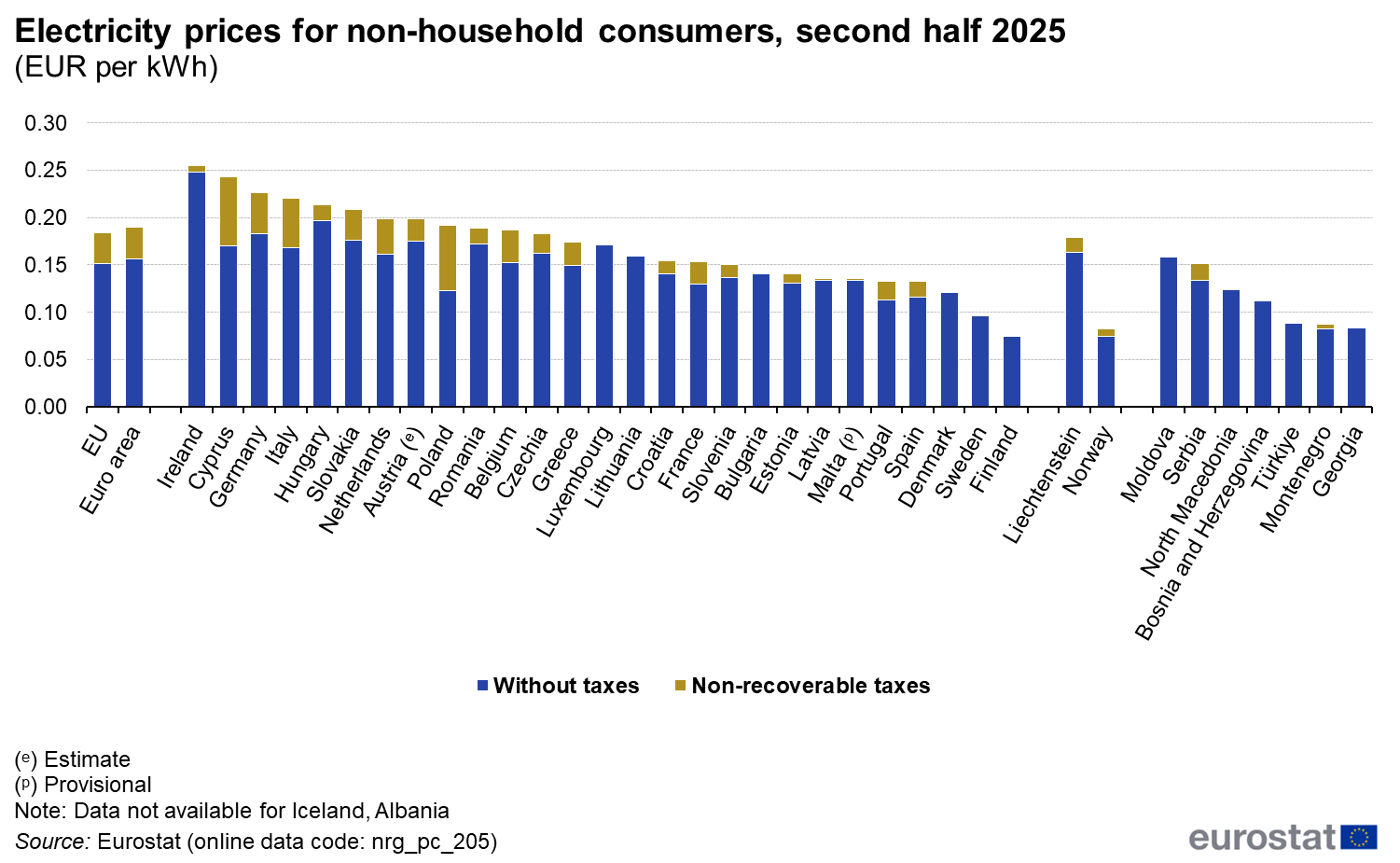

The result of closing German nuclear plants was exactly as the industry lobbyist predicted. Germany’s electricity costs have skyrocketed to the 5th highest in the world.

In 2025, German business electricity was the 3rd most expensive in the EU, pricing energy-intensive manufacturing out of the country.

The irony is brutal: industrial production is precisely Germany’s historical core competency. For decades, “Made in Germany” was the global gold standard for engineering excellence:

Premium automobiles: Mercedes-Benz, BMW, Porsche, Audi

Industrial machinery and machine tools, chemicals and pharmaceuticals: BASF, Bayer

Specialty chemicals, precision optics: Zeiss, Leica

Mittelstand: thousands of mid-sized, often family-owned manufacturers that quietly dominate global niches, from chainsaws (Stihl) to premium kitchen appliances (Miele) and power tools and industrial sensors (Bosch)

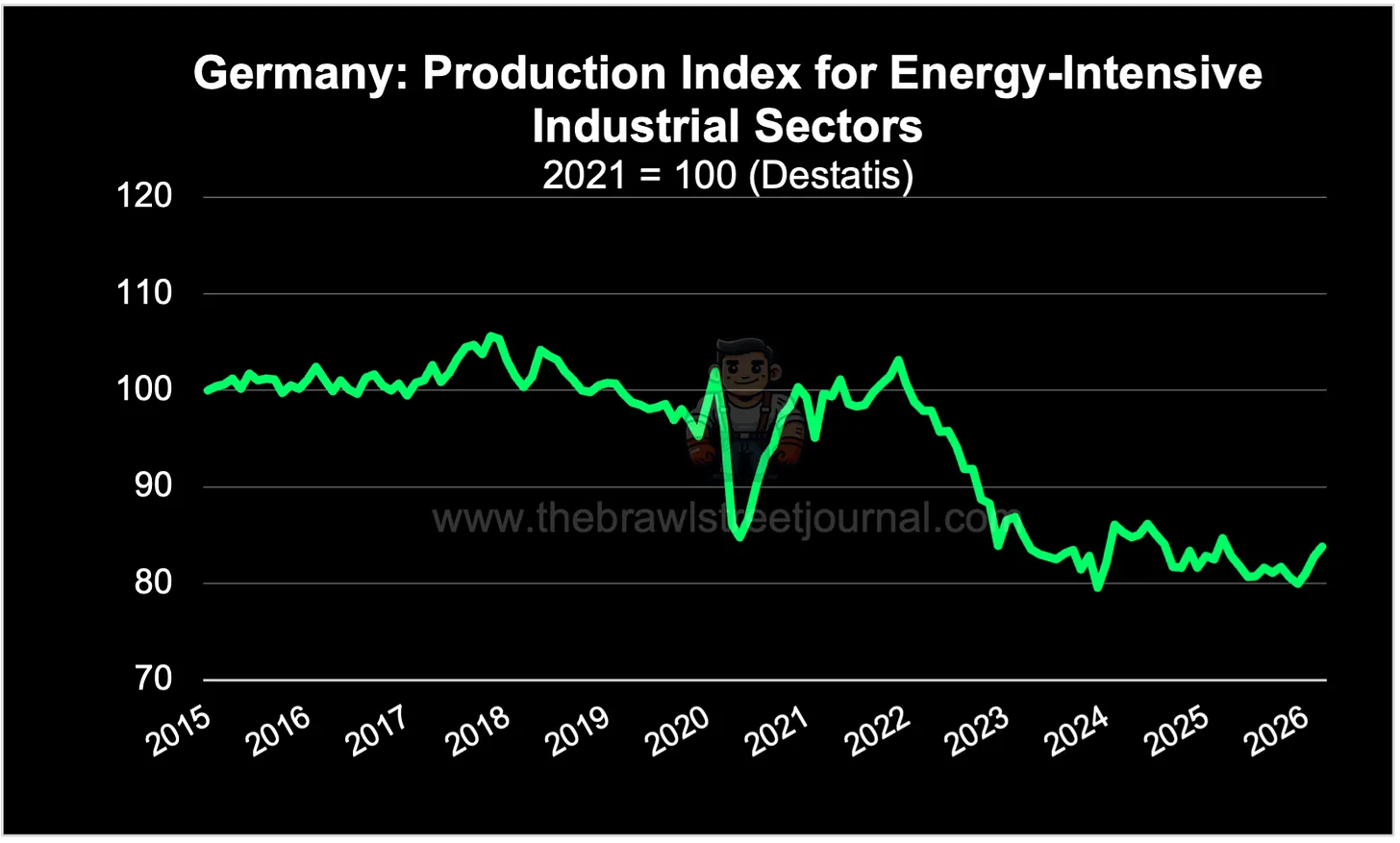

A coalition-driven energy policy has now made the most energy-dependent of these industries structurally uncompetitive on their home turf. Volkswagen closed one of its German plants for the first time in its 88-year history. BASF is adding new chemical capacity in China, where electricity is cheap and abundant. Steelmaker ArcelorMittal cancelled green conversion of existing plants, explicitly citing high German energy costs. As The Brawl Street Journal reported in June 2026, Germany’s energy-intensive industrial production is down 16% from 2015.

Germany took the one input its industrial base could not afford to lose (electricity) and made it one of the most expensive in the world.

The macro result is predictable. Germany has become the only major EU country to suffer back-to-back recessions in recent years; its economy contracted 0.9% in 2023 and 0.5% in 2024, with growth barely returning at 0.2% in 2025. Both manufacturing and exports are “down for the third year in succession”. Formerly Europe’s industrial engine, Germany is now the sick man of Europe.

In contrast to Germany’s multiparty parliamentary system, US states dominated by a single party don’t need to worry about election cycles; they can execute coherent multi-decade industrial strategy. What’s more, they can rely on other states, often on the opposite side of the political spectrum, to make up for their shortcomings. Nowhere is that dynamic more visible than in the contrast between America’s two largest state economies.

California and Texas: Opposite Politics, Outstanding Economies

The most powerful demonstration of the effectiveness of one-party states in America is the contrast between California and Texas, the world’s 4th and 9th largest economies if measured against nations. Nineteen of the fifty largest economies on earth are now US states.

California and Texas sit at opposite ends of the American political spectrum. Yet both have built world-class economies in their respective specialties, precisely because each has been free to compound a coherent set of policies for decades.

The Lone Star Energy Behemoth

Texas’ energy dominance reflects market-driven abundance rather than ideological allegiance to any single fuel source. Its deregulated, pro-development regime builds whatever is cheapest and fastest to deploy, which is why it leads in fossil fuels and renewables alike.

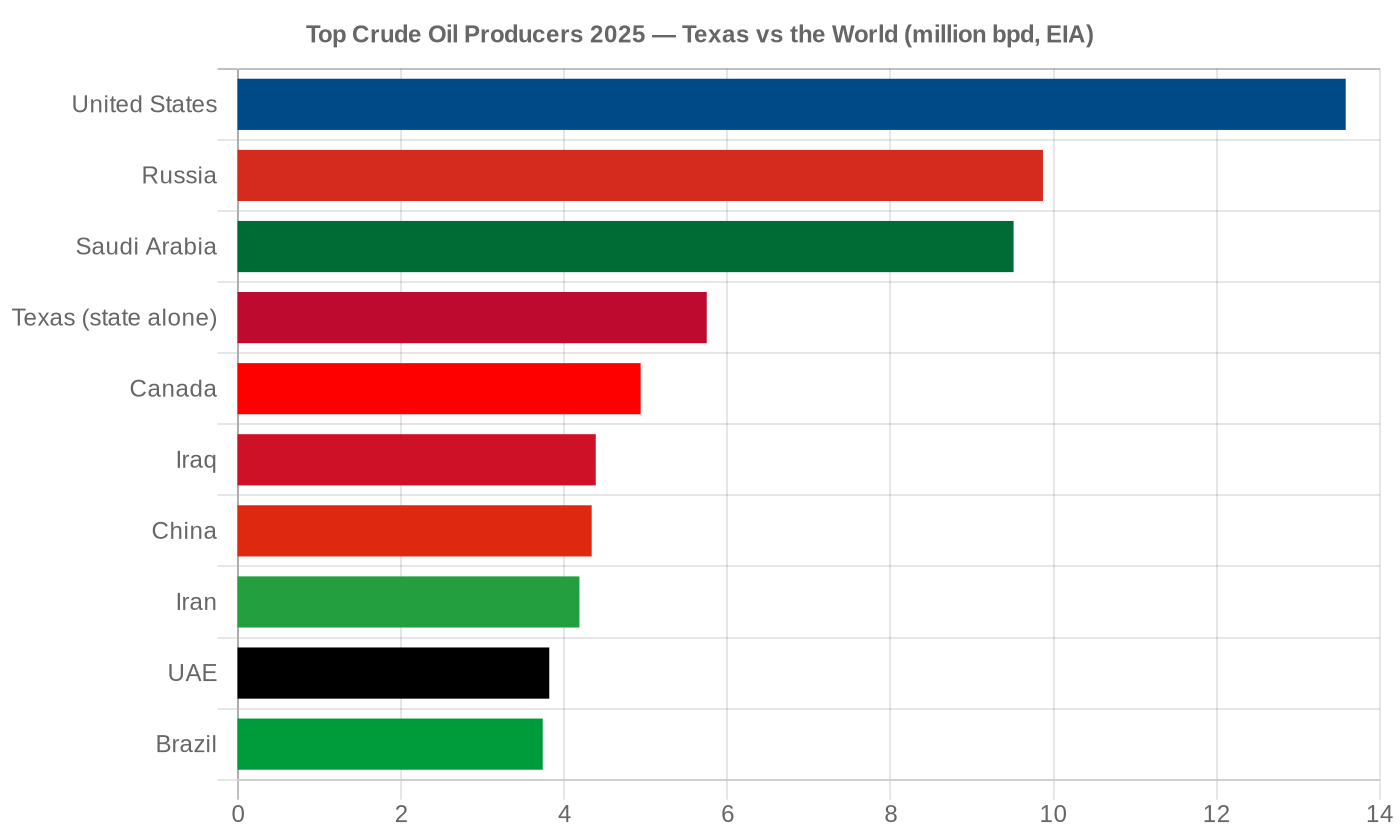

If Texas were a country, it would have ranked as the world’s fourth-largest crude oil producer in 2025, behind only the United States (including Texas), Russia, and Saudi Arabia.

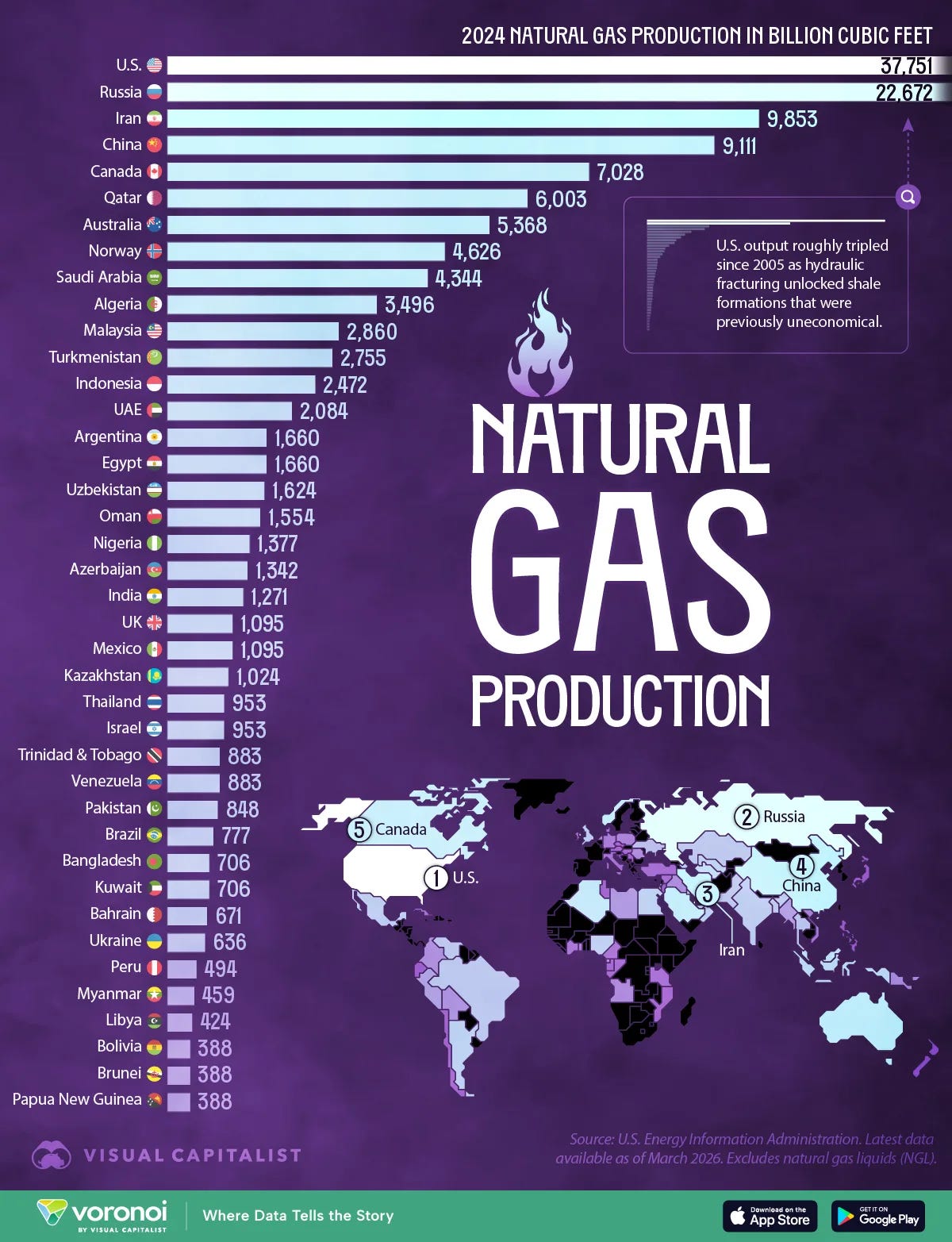

Even more impressively, Texas would have been the third-largest producer of natural gas in 2024, with 12 trillion cubic feet of production.

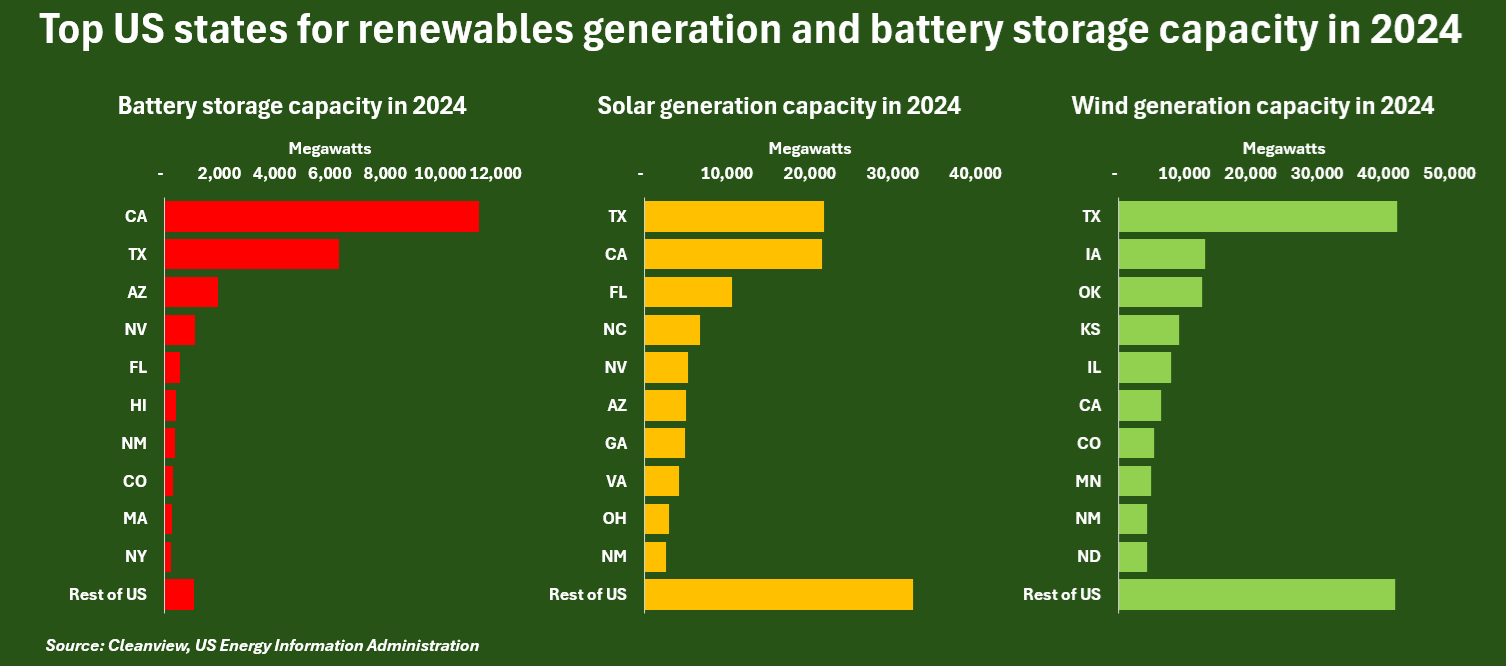

What’s really surprising about Texas is that the renewable buildout there now far exceeds the renewable energy generation capacity in every other state, even blue California.

Wind and solar combined met 36-40% of Texas grid demand through the first nine months of 2025. Texas didn’t embrace renewables out of a love for protecting the environment and the climate. It just freed up the private sector to chase the cheapest electron and in doing so, outbuilt everyone else (except China).

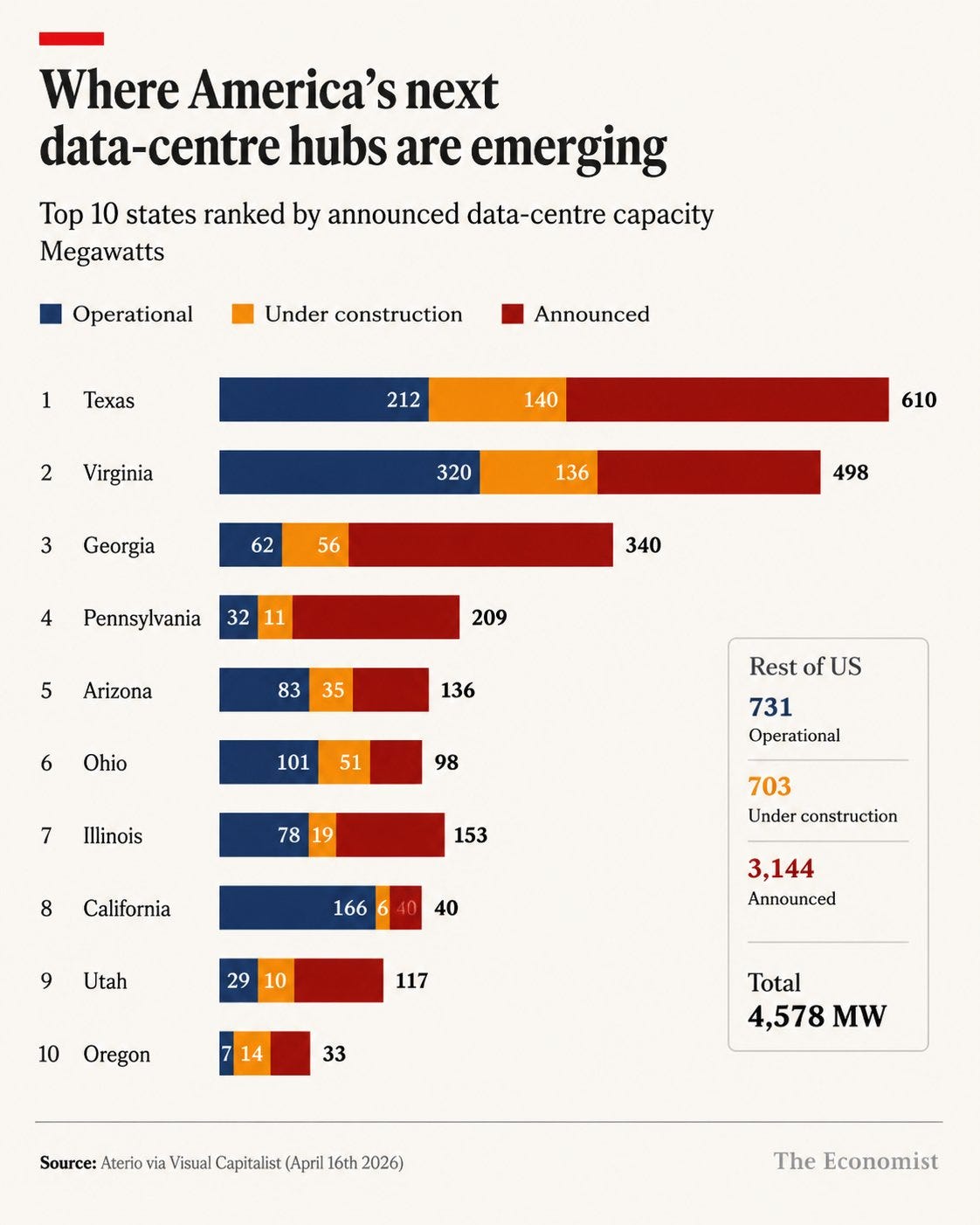

Texas’ energy abundance across both fossil fuels and renewables has positioned the state to dominate the next great industrial buildout: AI data centers. Texas is projected to overtake Virginia as the world’s largest data center market by 2030.

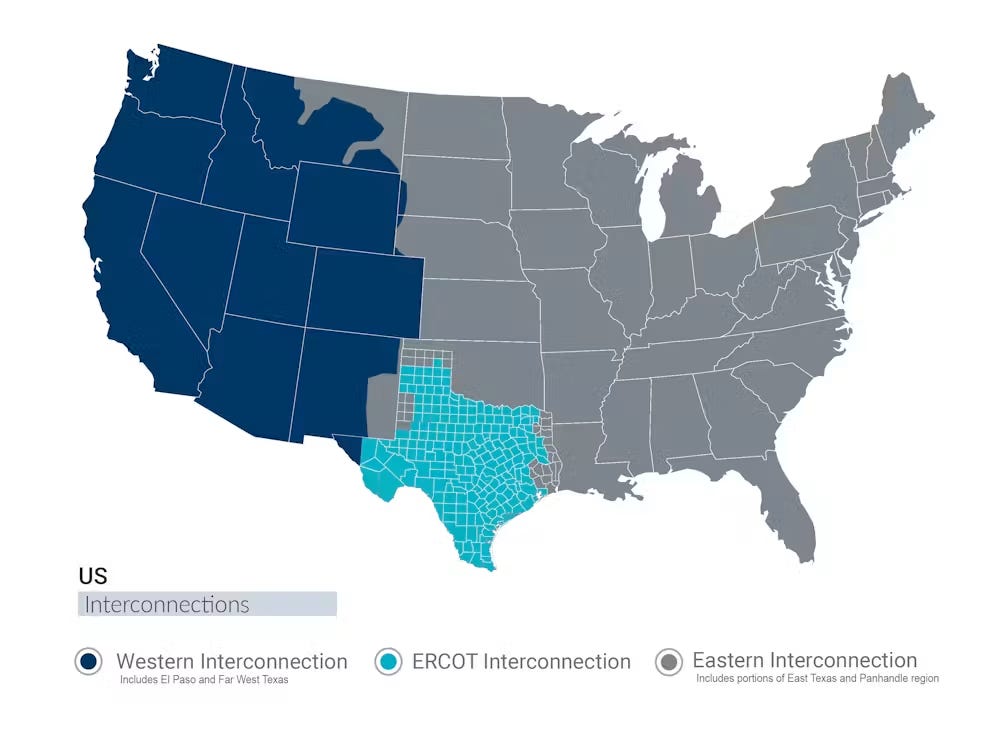

Texas’ independent grid is its unique advantage when it comes to electricity, which allows it to operate by far the most free-market approach in the country.

Texas is its own separated grid from the rest of the country. That makes it unique in the continental United States. It has chosen not to interconnect with the broader eastern and western grids that span most of the rest of the country, and it does so to avoid federal regulation. So the Federal Energy Regulatory Commission that regulates interstate electricity and gas markets has jurisdiction via the interstate commerce clause in the Constitution. And so by not participating in interstate trade in electricity, Texas carves itself out of that jurisdiction.

With US data centers waiting up to seven years for grid interconnections,

it’s easier to interconnect to the transmission system in Texas than it is everywhere else.

This explains why Big Tech is building out massive data centers in Texas. The Oracle-OpenAI Stargate flagship site is up and running in Abilene. Google is investing $40 billion in building Texas data centers. Meta is building a data center in El Paso whose energy consumption could be as much as the city of San Francisco.

The reason why Silicon Valley companies have chosen Texas for their data centers is brutally simple: data centers need power, Texas has the most abundant and cheapest power in the country, and Texas’ pro-energy, pro-business Republican governance enables it all.

But if these same tech companies wanted to hire the best talent, they’d have to go to California. The reason talent stays put in California is written into the state’s labor laws.

The Silicon Valley Flywheel

Unlike Texas’ pro-business governance, California is as pro-employee as it gets. The Golden State has had a near-total ban on noncompete agreements since 1872 and a statutory regime so hostile1 to post-employment restraints that California employers typically don’t impose gardening leave on California-based hires, even when they do so for the same roles outside California. That legal regime is the secret ingredient that transformed Silicon Valley from an agricultural hub in the 1960s into a global technology powerhouse.

In 1965, Cambridge, Massachusetts was the undisputed center of American high tech, with triple the number of technology sector employees as Silicon Valley. This made sense, given that Harvard and MIT were and still are two of the best research universities in the country. But Massachusetts’ noncompete-enforcing regime capped the potential of the best talent.

By contrast, California’s noncompete ban created a regional labor market in which engineers freely jump between rival firms. Talent moved to where it was treated best, and the cluster effect compounded within the Bay Area.

The story of Silicon Valley itself begins this way. In 1957, eight of William Shockley’s top researchers, the “traitorous eight”, quit his semiconductor lab to found Fairchild Semiconductor, a direct competitor. A decade later, two of those researchers, Robert Noyce and Gordon Moore, left Fairchild to found Intel. In any noncompete jurisdiction, none of those companies would have existed. The entire modern semiconductor industry traces back to a defection that California law made possible.

The same pattern repeats across generations. Apple was built in part by ex-Atari and ex-HP engineers, direct rivals in the early PC market. Google absorbed talent from Yahoo and Microsoft. Facebook recruited heavily from Google, most famously Sheryl Sandberg. OpenAI was founded with engineers drawn from DeepMind. Anthropic, in turn, was founded by former OpenAI employees and continues to attract talent from it.

In May 2026, Andrej Karpathy joined Anthropic having done zero gardening leave, waited through no cool-down period, and spent zero time on the bench while lawyers negotiated. California’s noncompete ban meant there were no legal handcuffs to slow him down. Frontier labs there compete for talent on mission, impact, compensation, and research opportunity, not litigation.

The contrast with other talent hubs is sharp. When professionals leave their jobs in New York, London, Hong Kong, or Singapore, they are routinely paid to do nothing for six to twelve months (gardening leave) before being allowed to join a rival. California courts treat this as a de facto noncompete, so employers there don’t use it.

The result: while professionals elsewhere spend a year of their prime career rotting on a beach, Californian employees are always building product and compounding skills.

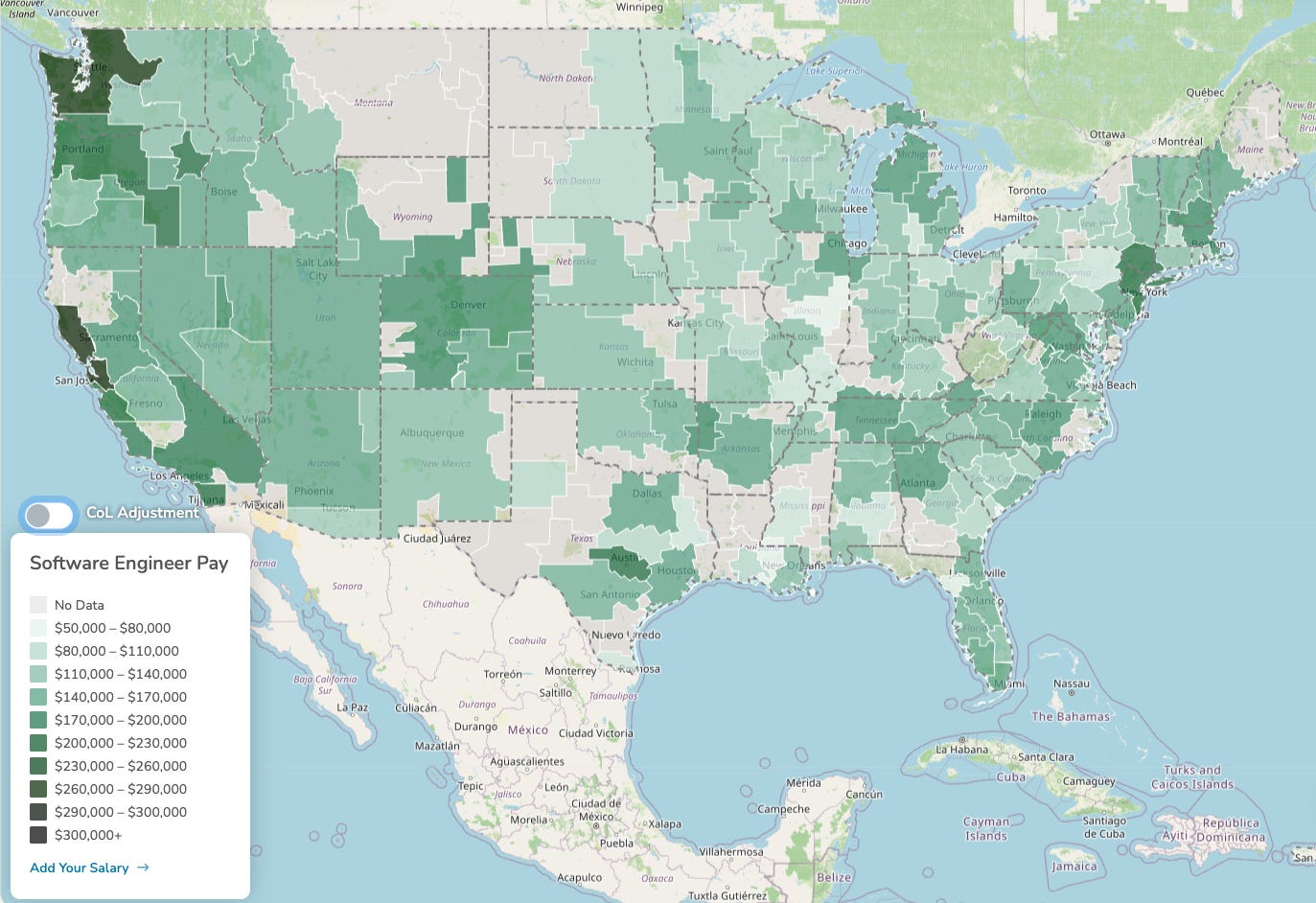

It’s little surprise then that engineering compensation in the Bay Area is so much higher than the rest of the country, which of course just attracts even more of the best talent.

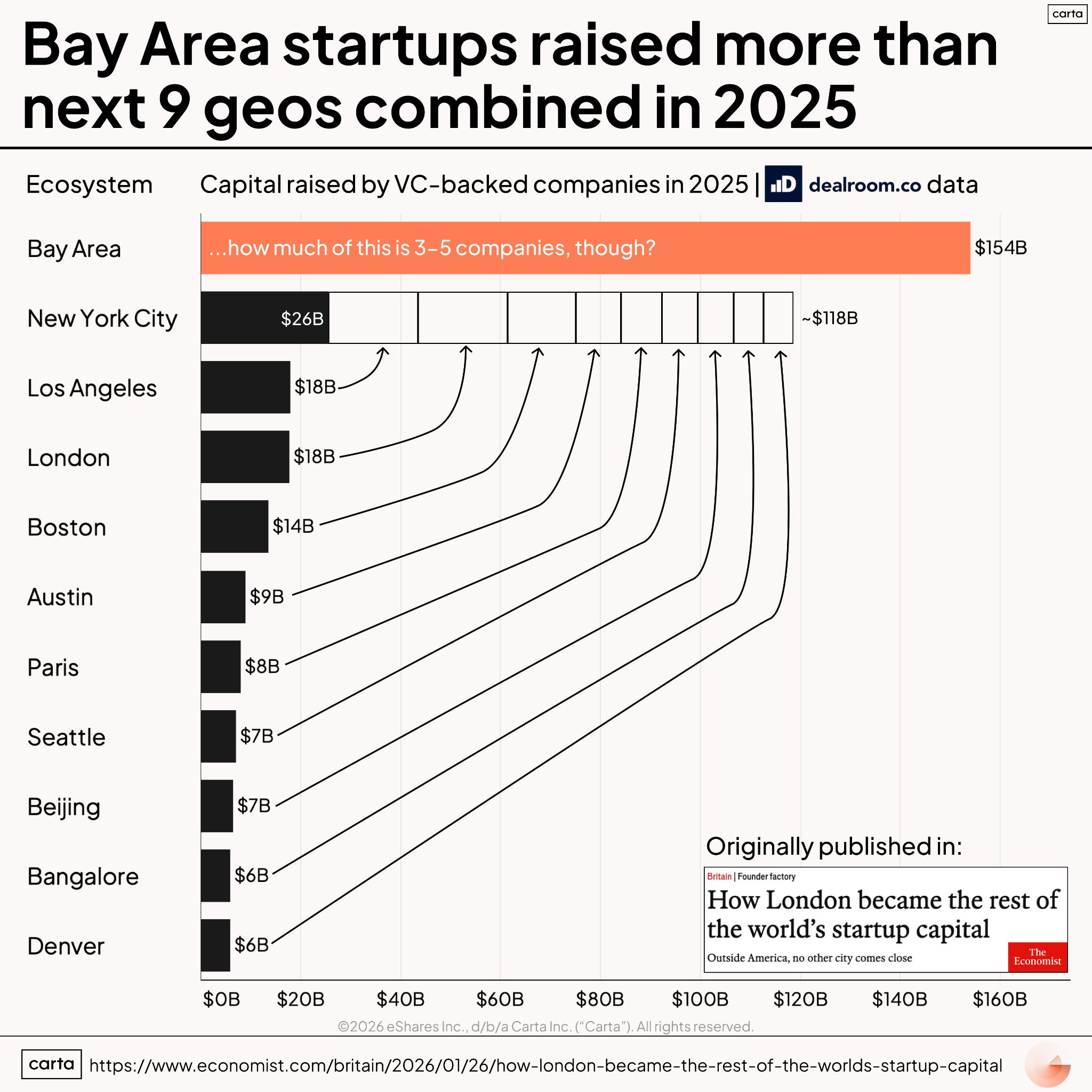

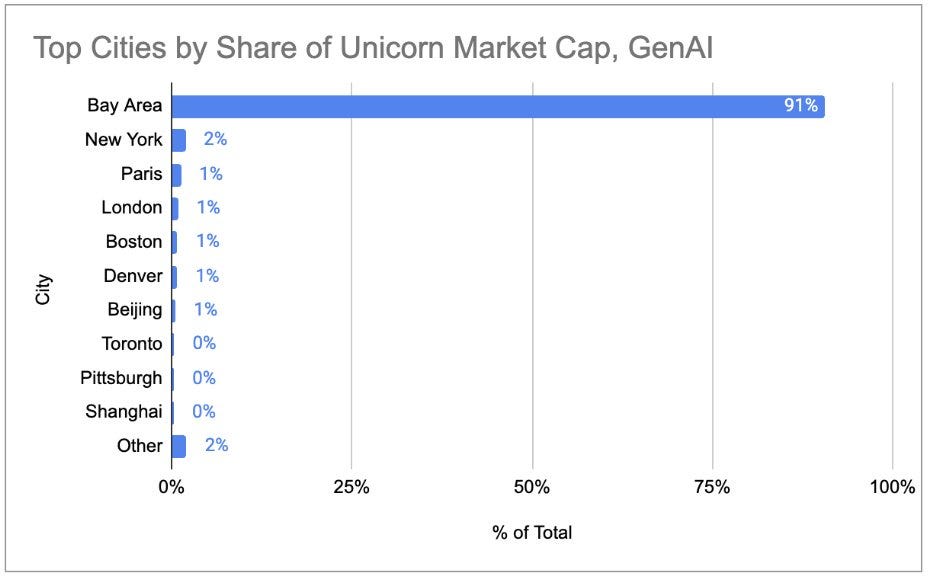

Given the sheer concentration of the best talent coupled with the most pro-employee regulations in the world, it goes without saying that the Bay Area remains the global tech capital by an astounding margin. Bay Area startups raised $154 billion of venture capital in 2025, more than the next nine cities combined.

The Bay Area holds 91% of the unicorn market cap in generative AI.

That concentration is no accident. As Aakash Gupta put it,

Research talent clusters tighter than engineering talent because research is a social output. The breakthroughs come from hallway conversations and coffee chats, not Slack threads. Remote work flattened software distribution. It made AI research concentration worse.

S players want to work with and be around S players. The talent has stayed in SV even as some of California’s wealthiest residents have left, a split that tells you which factor really drives the tech hub.

Why Bad Governance Can’t Break Silicon Valley

California has high taxes coupled with public services that, by any honest measure, are not great; homelessness and violent crime are higher in California than in lower-tax states.

Given that the quality of public services isn’t commensurate with the level of taxes they pay, the rich are rightfully angry at the prospect of a billionaire wealth tax slated for the November 2026 election. Larry Page, Sergey Brin, and Mark Zuckerberg have already moved their tax residency from California to Florida.

If the wealth tax passes, the most plausible casualties are

Loss of capital gains tax revenue from some of the world’s richest men

Supervoting share structures to ensure founder control, which would become punitively expensive to pay, as the wealth tax would be calculated based on voting power, not economic value.

Although capital is happy to migrate out of California, the vast majority of tech talent has not moved, will not move, and has in fact returned from Texas and Florida, which continue to allow noncompetes, unlike California’s total ban on them.

Notably, Jensen Huang, who holds no supervoting Nvidia stock, has publicly shrugged at the California billionaires tax, explicitly citing the quality of talent in Silicon Valley as his reason to stay.

The lack of a complete ban on noncompetes will prevent Boston, NYC, Miami, and Austin from ever catching up to Silicon Valley, regardless of favorable tax policies.

Silicon Valley won’t move to Miami anytime soon

In 2020, Miami mayor Francis Suarez’s offer to help a Silicon Valley venture capitalist move SV to Miami went viral on Twitter.

Used to being treated poorly2 by politicians in California, Suarez’s pro-business attitude was a breath of fresh air for Silicon Valley founders and VCs. Unfortunately, Miami’s potential as a rival to Silicon Valley was short-lived.

In 2025, Citadel successfully lobbied Florida’s pro-business legislature to pass the CHOICE Act, which enables noncompetes to

Last up to four years, double the previous two-year limit

Be enforceable globally, i.e. the only way to fully avoid enforcement is to move somewhere that outright bans noncompetes, like California

Apply to employees outside Florida who are working for companies based in Florida

The CHOICE Act is the final nail in the coffin: Silicon Valley will never move to Miami.

Talent has returned to the Bay Area in spite of San Francisco’s well-documented street disorder and visible homelessness because the next Andrej Karpathy is only going to work in a place with zero limits on the potential of the best talent.

The massive and growing concentration of talent in Silicon Valley forms a self-reinforcing flywheel: talent attracts capital, capital attracts more talent, and each turn makes the next turn easier. That flywheel now dwarfs poor state policymaking and governance.

Red or Blue, Every State Builds (Sometimes, Together)

As shown by the strength of California and Texas economies and the specific underlying policies, under the American federal, two-party system, each state effectively becomes a one-party state with the freedom to compound its comparative advantages into dominant, unassailable flywheels, so much so that bad presidents can’t change America’s trajectory.

This is exactly the kind of resilience Nomad Capitalist denies America possesses.

California and Texas could not be more different politically, yet each needs the other to prosper. California companies’ data centers need Texas energy; Texas’ energy industry needs California capital and software talent to create the AI workloads that justify the energy buildout. As evidenced by Florida’s CHOICE Act, Texas’ pro-business legislature would never ban noncompetes to supercharge its tech industry. California’s environmentally conscious and NIMBY legislature would never truly develop the state’s ample energy potential.

The two states help each other through trade and need each other to prosper. That is the federal model at its best. The relentless cycle of partisan conflict playing out in Washington, across news cycles and social media feeds, and around the Thanksgiving dinner table serves as a distracting, loud background noise that blinds the casual observer to the actual engine of American prosperity.

A skeptic will say that American outperformance was driven by software, the internet, and shale, not by electoral structure, but that gets the causation backwards. Each of those booms was enabled by state governments with the policy continuity to sustain decades-long bets. California’s permanent ban on noncompetes built the talent density behind software and the internet. Texas’ durable pro-development regime made the shale revolution possible.

The US dollar is strong for the same reason. A reserve currency is only as good as the economy backing it, and that economy is the sum of these compounding state economies. The electoral structure is upstream of all of it because it is what lets a single party govern a state long enough to compound an advantage in the first place.

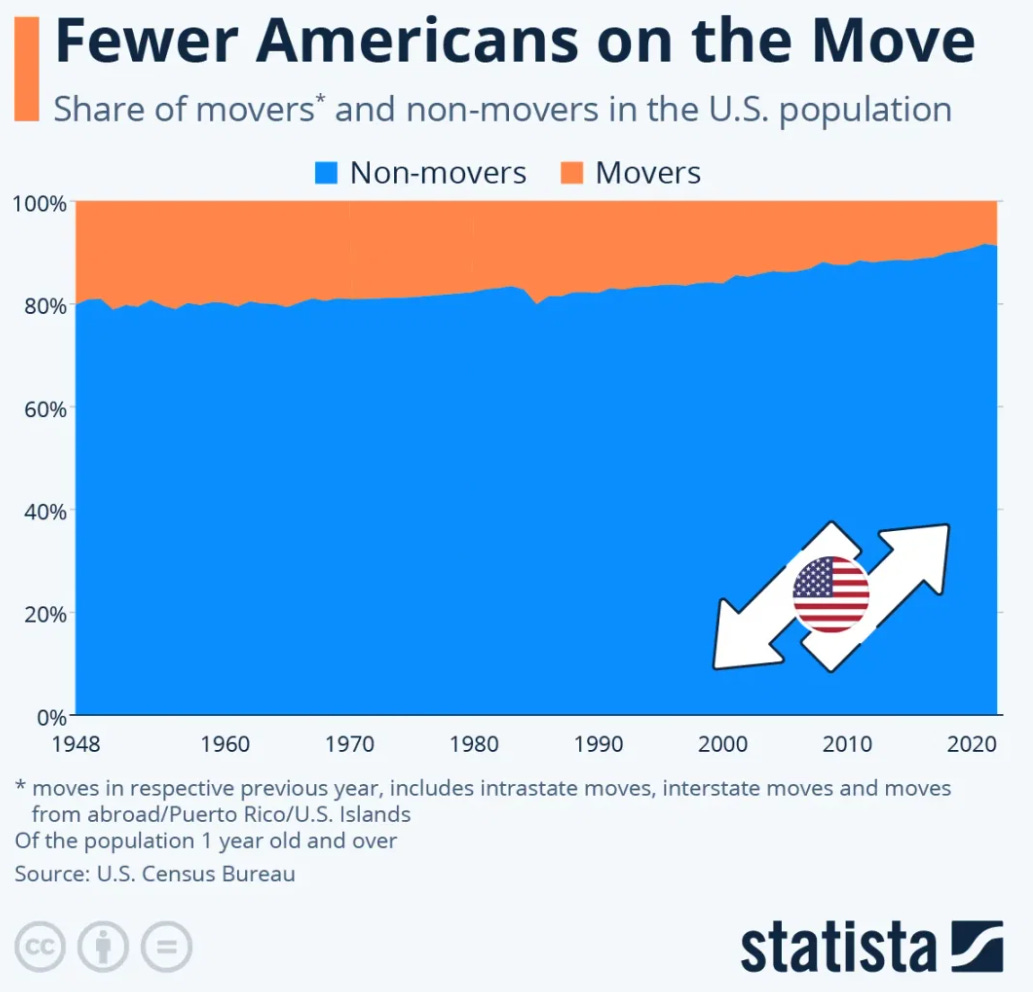

Americans Are Staying, but Shifting States

If the structure is this strong, you would expect Americans to back it with their choices, and they do. Nomad Capitalist’s motto is “go where you’re treated best.” Americans are doing exactly that, but the data falsifies his thesis that the right move is to leave the United States.

In spite of claims that they’ll leave if their favored presidential candidate loses, fewer Americans are moving than in the past.

When Americans vote with their feet, they overwhelmingly stay inside America. In 2024, 7.1 million of them moved to a different state. By contrast, just 104,000 U.S. citizens emigrated to OECD countries the previous year. Americans are not leaving the country; they are shopping between its fifty competing jurisdictions.

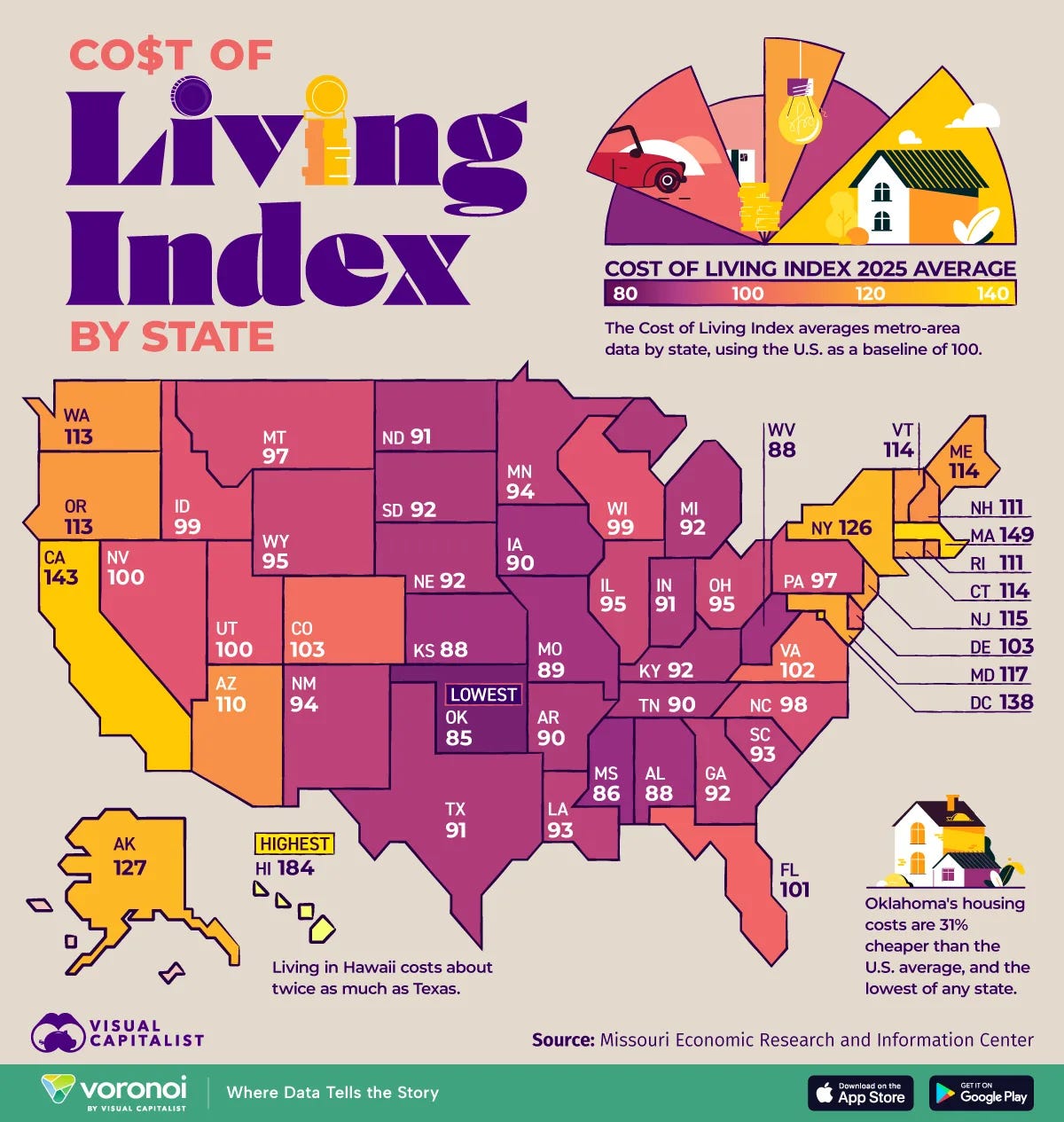

Unaffordable cost of living is a serious problem that is overwhelmingly concentrated in coastal blue states. On the Cost of Living Index (US = 100), Hawaii tops the nation at 184 and California sits at 143, while Texas is below the national average at 91. In other words, living in Hawaii costs twice what it does in Texas.

This has created a bifurcated migration pattern. While elite engineering and research talent remains anchored to the Bay Area to maximize their career potential, the broader workforce is voting with their feet.

Millions are moving to parts of the country where they get more bang for their buck, escaping the unaffordable cost of living in coastal blue states, without surrendering their access to the largest single market, the deepest capital markets, and the world’s deepest entrepreneurial ecosystem.

This is the killer point Nomad Capitalist misses. Inside the United States, a Florida resident pays less tax, faces a benign business climate, and still gets to sell into a $30 trillion economy, raise from American VCs, and litigate under a familiar common-law legal system in English.

Going to Malaysia, Mexico, or Serbia delivers tax benefits but at the cost of leaving the world’s most lucrative market and capital base. Most Americans correctly conclude they can capture >80% of the same benefit without losing much by moving from California to Texas. That domestic migration is the move most Americans are actually making.

America’s Entrepreneurial Spirit

In his video on selling all his US investments, Nomad Capitalist said,

This idea that S&P 500 and the broader US stock market or Berkshire Hathaway is going to capture global exposure, I don’t align with that. I don’t think it’s true. I think that American companies will lose share.

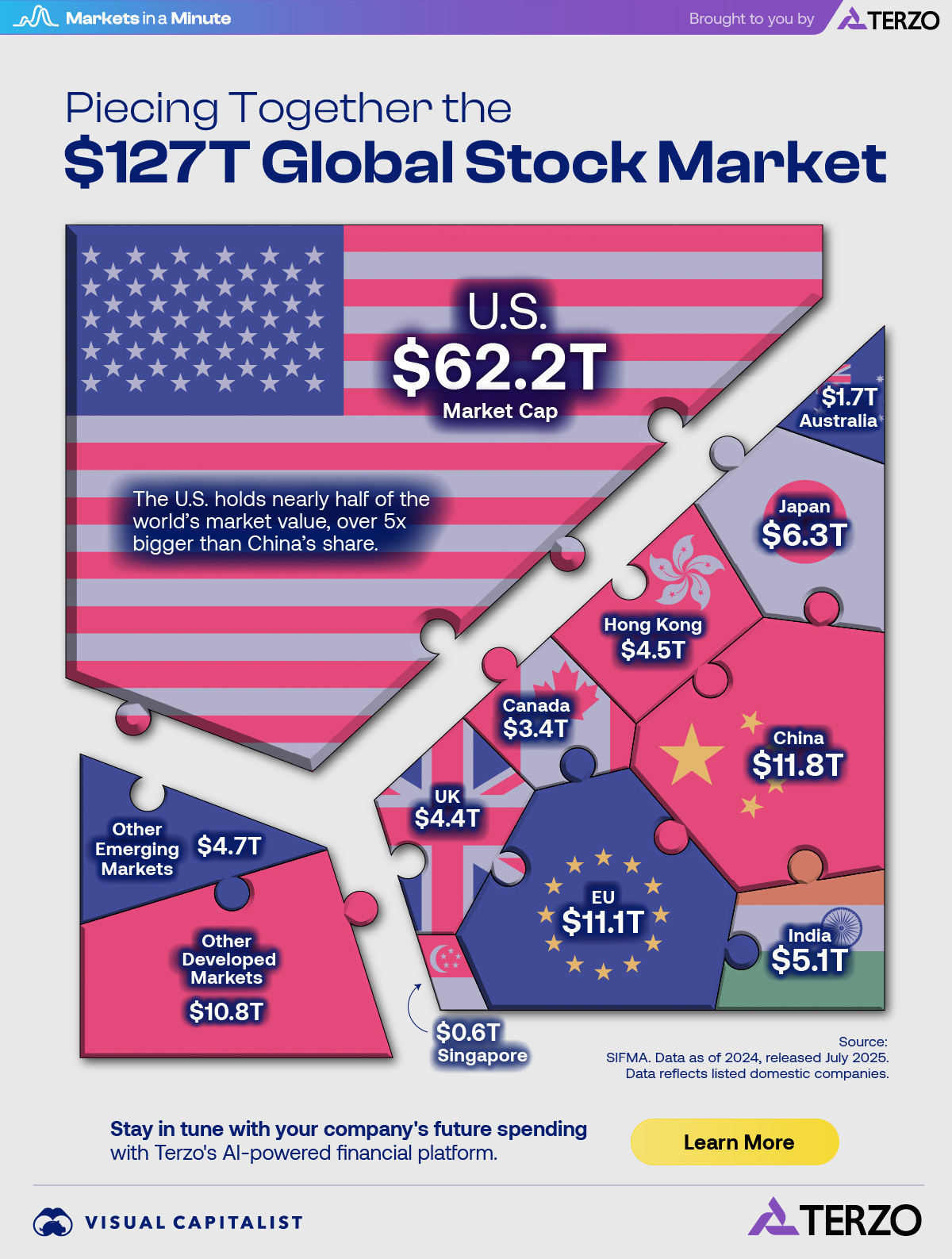

The problem is that global investors strongly disagree. Although the US accounts for 4% of global population and 26% of GDP, its companies account for more than half of global market cap and more than the next eight countries combined.

Even the harshest critic must concede the strength of the underlying economy, the depth and dynamism of US companies, the entrepreneurial spirit, and the capital markets.

That entrepreneurial spirit is no accident; it springs from a culture that rewards risk-taking. Silicon Valley has a distinctive cultural belief that failure is the stepping stone to future success. This fuels constant experimentation, which, when coupled with the free enterprise system, has powered and will continue to power American economic success.

A 1% excise tax on stock buybacks, small enough to be a rounding error, hasn’t changed this and won’t. Its logic is also sound: dividends are taxed, while buybacks let investors defer capital gains by holding longer, so the tax simply narrows that gap.

Neither will golden shares, the newest iteration of the established idea of governments owning significant stakes in critical national enterprises. The #1 most economically free country of Singapore is ruled by a government that owns major stakes in DBS, Singtel, and Singapore Airlines.

American economic momentum doesn’t live in Washington. It compounds in companies, states, and capital markets, which is why it has thrived under every kind of president the country can produce, including the ham sandwiches.

No Country is Without Problems, Of Course

America has plenty: crime, decaying infrastructure, inequality (including homelessness, healthcare, and oligopolistic market concentration), and cost of living. These are real problems, and they make millions of American lives worse. But inequality is a global problem in the AI era, not an exclusively American one.

The country is starting to self-correct. Crime is down. Red states are attacking housing costs and homelessness by building. Doctors are increasingly bypassing insurance for out-of-pocket payments; this direct care model reduces administrative overhead and lowers healthcare costs. Infrastructure still isn’t being taken seriously. Oligopolistic concentration is getting worse, but it is exactly the kind of problem a future populist president (someone like Lina Khan, AOC, or Bernie Sanders) could take on with a Teddy Roosevelt-level impact. As with the Gilded Age, a country can have a booming economy and serious social problems at the same time.

Here the federal model is itself the remedy: with fifty jurisdictions running parallel experiments, some state is always piloting a fix, and the ones that work reap the rewards. Texas builds housing; California builds an innovation cluster. America runs fifty experiments, and the most effective ones stand the test of time.

A Ham Sandwich Every Four to Eight Years: The Bargain That Works

Seen this way, the presidency matters far less than either side fears. This framing should change how voters on both sides of the aisle feel about each other. Democrats and Republicans tend to view the other party as an existential threat to the country and see every presidential election as the one that finally breaks America.

But the data tells a different story. Throughout the terms of all of the living presidents (Clinton, Bush, Obama, Trump 1, Biden, and Trump 2), the US economy kept growing, US states kept compounding their advantages, and the gap between American and European prosperity kept widening. Whichever party held the White House, the country got richer.

The reason is that the two parties have, without intending to and often while loudly hating each other, been collaborating on building a collectively stronger country.

Decades of continuous Democratic governance provided the stability for California’s tech ecosystem, Massachusetts’s biotech cluster, and New York’s financial markets to organically compound. Uninterrupted Republican governance gave Texas the runway to build an energy behemoth, Florida to become a capital magnet, and the Sun Belt to launch a manufacturing renaissance. Neither side could have incubated what the other side did.

More importantly, neither side has been able to stop the other side from building. The result is a country with simultaneously the world’s most dominant software industry, top oil and gas industry, deepest capital markets, and premier research universities; no other country has this combination.

The bargain is this: every four to eight years, one side has to swallow hard and accept that someone they consider a ham sandwich is going to occupy the Oval Office. But 250 years of constitutional design and the organic divergence it produced have made the federal government largely irrelevant to where prosperity really comes from.

A ham sandwich cannot dismantle California’s tech flywheel or Texas’ energy flywheel. The ham sandwich gets to make speeches, sign executive orders that the next administration will reverse, and hold press conferences watched by millions. The compounding happens at the state level, in companies, in capital markets, and in research labs, regardless of who is president.

So the next time hardliners on either side of the aisle find themselves convinced the other half of the country is destroying America, they should consider the alternative hypothesis: the other half is quietly building the parts of America that their own half cannot build. Hating the other side is optional. The collaboration is happening anyway, and everyone benefits from the result.

Why the End of the Unipolar Moment Is Bullish for America

With the domestic economy insulated by the federal architecture, the harder question becomes external. Tech investor and presidential advisor David Sacks recently captured the prevailing anxiety in Washington regarding China:

The United States does not tolerate peer competitors. We want to be the number one country. We want to be the most powerful country. The balance of power is to some degree a zero-sum game. Economics are not, but power is. The history of the United States is we want to be number one and we don’t like having peer competitors. And I mean that’s the bottom line.

Sacks is right that America wants to be number one, but his framing misses a crucial historical reality. For most of its history, the United States thrived precisely because it had peer competitors to push against (from the British Empire to the Soviet Union); these rivals forced America to constantly step up its game. The US might not like having peer competitors, but it needs them.

The actual historical anomaly was not the Cold War; it was the unipolar holiday that followed. From the fall of the Soviet Union to the rise of China, America lacked a peer entirely, and unchallenged countries get lazy. While the United States generated unprecedented wealth during this unipolar era, that economic boom was highly asymmetrical: the country dominated the digital and financial realms while allowing its physical industrial base to hollow out.

This complacency defined the 2010s, prompting Peter Thiel to famously lament the lack of physical innovation with his tagline:

We wanted flying cars, instead we got 140 characters.

This is exactly why the return of great-power competition is the most bullish development for the United States in a generation. The zero-sum battle for geopolitical dominance inevitably forces a positive-sum explosion in technological advancement.

The existential pressure of a true economic peer has catalyzed a massive reallocation of American capital and engineering talent away from trivial pursuits and toward hard technology. The complacency of the 2010s has been replaced by a domestic industrial renaissance across defense technology, aerospace, artificial intelligence, and semiconductor manufacturing. By forcing the United States to compete for its position at the top of the global hierarchy, China has reawakened one of the most potent innovation machines in history.

The Limits of Force, and the Case for Statecraft

There is a second, less obvious reason to be bullish on America: Washington has learned the limits of its military power. The Iran war did not achieve Washington’s objectives, and that failure may turn out to be one of the most valuable lessons of the post-unipolar era.

The Iran episode points in a direction future commanders-in-chief are likely to notice: America’s adversaries can now wield significant economic leverage. When the target of American military power can choke a strait carrying a fifth of the world’s oil supply, the costs of war show up immediately in energy prices, shipping rates, and voter anger.

That single shift, internalized across both parties, is worth more to American prosperity than any specific foreign policy doctrine. It frees up an enormous amount of national energy, talent, capital, and political bandwidth that would otherwise be consumed by wars of choice.

What replaces force in a bipolar world is diplomacy and economic statecraft. Sending the president to Beijing to work out a mutually beneficial deal will be far more effective than sending young Americans to die far away from home. The leverage available through this channel is enormous: when the two superpowers actually agree on something, nobody else can stand in their way. That is the true geopolitical prize of US-China co-opetition. The two countries do not need to like each other or even trust each other to recognize that aligned interests create an insurmountable global consensus.

The dividend of this shift is domestic. Every dollar not spent on a war of choice, every hour of presidential attention not consumed by a foreign quagmire, and every young American not sent overseas to die is a resource freed up to solve the problems that actually shape American livelihoods: housing, healthcare, education, energy, immigration, and industrial capacity. The end of the unipolar moment is not just bullish for America because competition forces the country to step up its game. It is bullish because, for the first time in a generation, America can stop trying to run the world and start finishing the job of building and strengthening itself.

Epilogue: US-China Co-opetition Is What the World Needs

America has a peer competitor again, but that doesn’t mean America is destined to lose. If anything, peer competition is the cure for the unipolar complacency that produced Twitter instead of flying cars. The US, forced to compete again, will respond the way it always has when challenged: by innovating. The existential drive to win forces a massive escalation in capability, which ultimately drives economic development and technological improvement for the entire globe.

Fifty one-party states in a federal system and one unitary, centralized state. Two superpowers competing and succeeding in their own way.

A ham sandwich can run the federal government, fifty one-party states can each compound their own flywheel for decades, and those fifty economies can trade with and offset one another’s weaknesses, allowing America to keep succeeding.

About

Inverteum Limited (HK) is a trading firm that specializes in long-short algorithmic strategies to generate returns in both bull and bear markets.

Inverteum has generated 50%+ annualized returns since inception.

How We Invest

Minimize allocation to individual stocks due to their unpredictability.

Build a strategy designed to harness the market’s momentum, with the tactical agility to pivot and capitalize on downward trends when necessary.

Be prepared for bear markets and ensure profitability during bad times by implementing a short selling component to the strategy.

In Edwards v. Arthur Andersen (2008), the California Supreme Court held that even “narrow restraints” on future employment are incompatible with the text of Section 16600, and reaffirmed the state’s public policy in favor of employee mobility.

“There is an attitude that has been expressed by some leaders that says, ‘We don't want you and we don’t need you,’” Suarez said, alluding to how business owners say they feel they are being treated in Silicon Valley. "It's the opposite of the 'How can I help?' attitude, 'How can I grow this ecosystem?'"

Hilarious and weirdly patriotic. God bless this fucked-up country, nowhere else compares

This is the most convincing version of the federalism-as-moat argument I've read. What I'd add from where I sit tracking India and other emerging markets at MarketMind is that this is precisely the structural advantage most EM economies lack. A country can have brilliant individual policy, but without credible commitment to multi-decade continuity at the sub-national level, the policy gets reversed before the compounding shows up. The US doesn't need its federal government to be competent, it needs fifty governments where enough of them stay competent long enough to compound.